In Summary

- Rising global interest rates and weak currencies have pushed debt burdens to historic highs across parts of Africa.

- Countries with long-standing structural deficits, repeated external shocks, and limited export diversification dominate the 2026 debt rankings.

Deep Dive!

Wednesday, 21 January 2026. Africa’s debt debate is often framed as a single continental problem, yet debt outcomes vary sharply from country to country. While some governments have managed to restrain borrowing or benefit from relief initiatives, others have entered 2026 with public debt levels that now exceed the size of their economies.

Measured as total public debt relative to gross domestic product, debt-to-GDP ratios reveal how much pressure governments face in financing spending, servicing obligations, and maintaining basic services. This ranking is based on the latest IMF Debt Sustainability Analyses, World Bank International Debt Statistics, and 2024 to 2025 national budget and treasury reports, with projections extended into 2026.

The countries appearing in this list share several traits. Many inherited fragile economic structures at independence, relied heavily on external financing for development, or experienced prolonged political instability, conflict, or repeated commodity shocks. Over time, borrowing intended to support growth gradually accumulated into large debt stocks that now weigh heavily on economic performance.

The ranking is based on gross public debt as a share of GDP, using projections and estimates available up to late 2025 and early 2026. Data is drawn from the International Monetary Fund, World Bank, African Development Bank, national treasury publications, and central bank reports. Where official figures vary, median estimates are used to reflect a broader consensus.

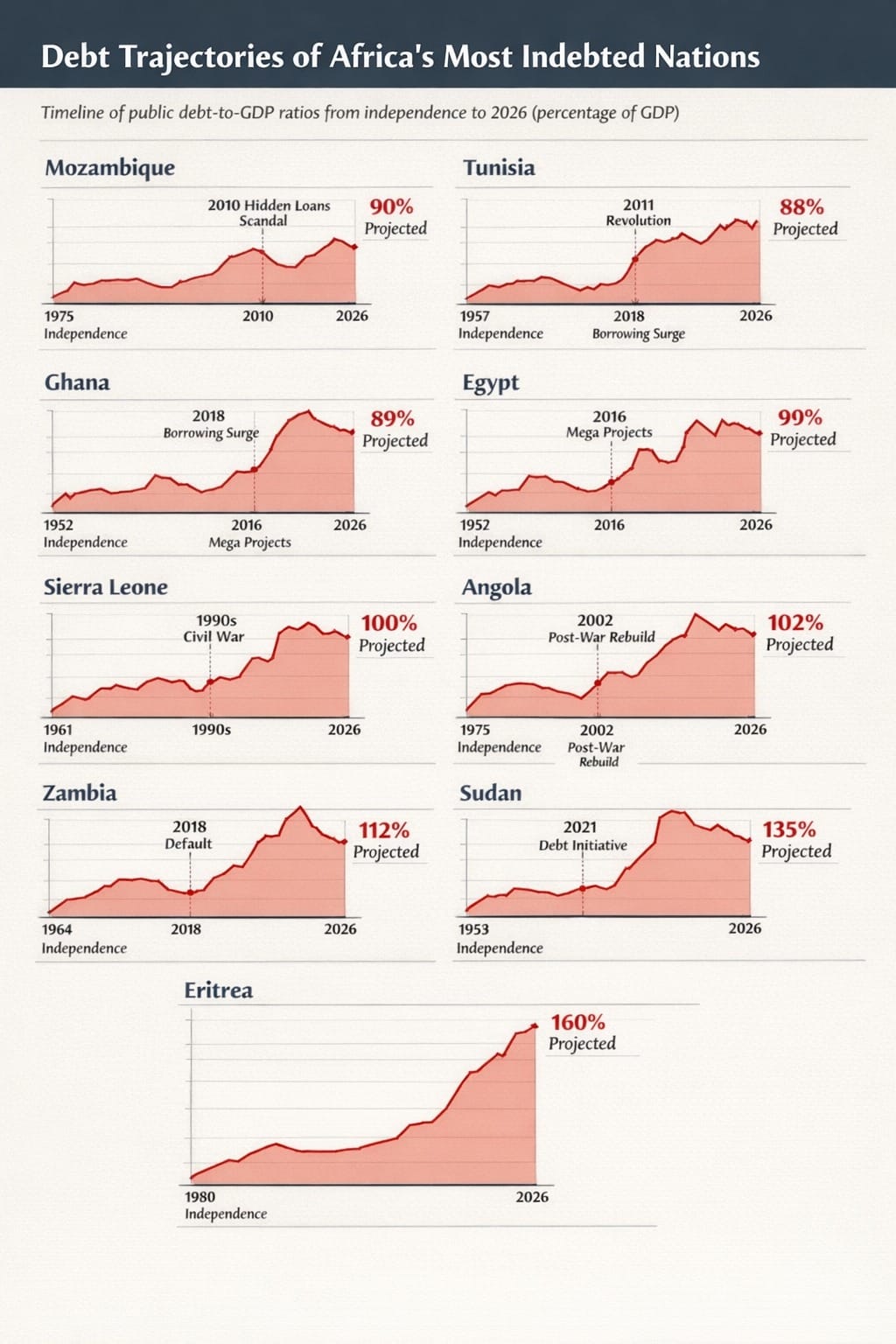

Tracking Africa’s public debt in 2026: This infographic shows the debt-to-GDP ratios of the continent’s most indebted nations, revealing trends, pressures, and the impact on economic stability.

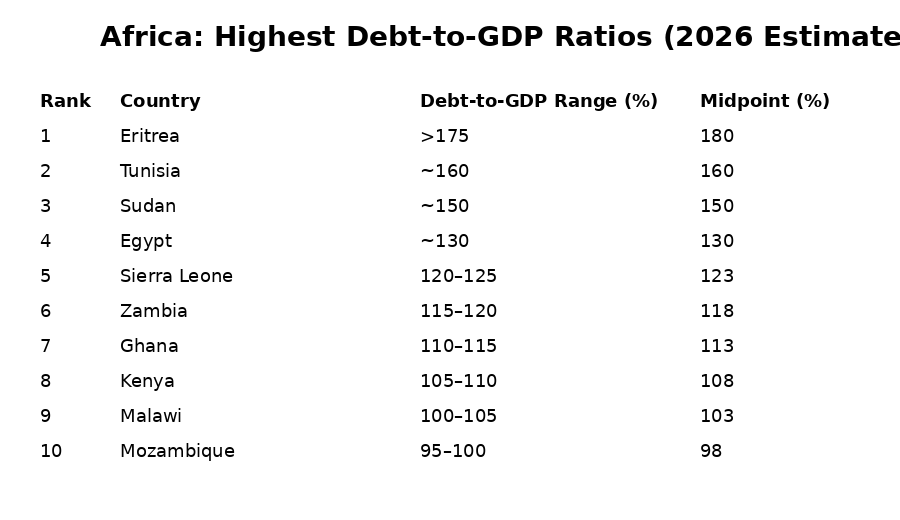

10. Mozambique

Estimated debt-to-GDP ratio in 2026: about 95 to 100 percent. Mozambique’s debt challenge traces back to its post-independence years after 1975, when the country emerged from Portuguese colonial rule with limited infrastructure and institutional capacity. Early borrowing focused on rebuilding transport corridors, ports, and power generation, especially along the Zambezi basin. However, progress was repeatedly interrupted by a long civil war that ended in the early 1990s.

Debt pressures intensified after 2013, when previously undisclosed government-backed loans linked to maritime security and tuna fishing came to light. The revelation damaged investor confidence and shut Mozambique out of affordable international financing. At the same time, expectations around offshore natural gas projects encouraged borrowing for future revenues that were repeatedly delayed.

By the early 2020s, Mozambique was servicing debt while still waiting for large-scale gas exports to fully materialize. Security challenges in Cabo Delgado further strained public finances, forcing the government to rely on external support. By 2026, Mozambique’s debt will remain elevated, reflecting a country still caught between long-term resource potential and short-term financing pressures.

9. Malawi

Estimated debt-to-GDP ratio in 2026: about 100 to 105 percent

Malawi’s borrowing history is closely tied to its agricultural economy and repeated climate shocks. Since its independence in 1964, the country has relied heavily on external financing to support food security, rural infrastructure, and social services. Tobacco exports, long the backbone of foreign earnings, failed to keep pace with population growth and import needs.

Debt rose steadily in the 2000s as Malawi expanded fertilizer subsidy programs to stabilize food production. While these programs improved short-term yields, they placed persistent strain on public finances. Currency devaluations and rising import costs for fuel and farm inputs further widened financing gaps.

By the early 2020s, Malawi faced mounting repayment obligations alongside recurring droughts and floods. External support helped prevent immediate default, but borrowing continued to cover basic budget needs. By 2026, Malawi’s debt-to-GDP ratio reflects a fragile economy where social protection, climate vulnerability, and limited export diversification intersect.

8. Kenya

Estimated debt-to-GDP ratio in 2026: about 105 to 110 percent

Kenya’s debt build-up is rooted in an ambitious development agenda pursued since the early 2000s. After decades of underinvestment following independence in 1963, the government expanded borrowing to modernize transport, energy, and urban infrastructure. Major projects included standard gauge railways, highway expansions, and power generation upgrades.

Much of this borrowing occurred between 2013 and 2019, financed through a mix of bilateral loans, commercial bonds, and multilateral funding. While infrastructure capacity improved, returns were slower than projected, and revenue growth struggled to match repayment schedules.

External shocks during the early 2020s, including global supply disruptions and currency pressure, increased servicing costs. By 2026, Kenya will remain one of East Africa’s largest economies, but its high debt-to-GDP ratio highlights the challenge of balancing long-term development goals with near-term repayment demands.

7. Ghana

Estimated debt-to-GDP ratio in 2026: about 110 to 115 percent

Ghana’s debt journey reflects cycles of optimism tied to natural resources. Following independence in 1957, the country invested heavily in industrialization and energy, including the Akosombo Dam. Debt relief initiatives in the early 2000s temporarily eased pressure, offering a fresh start.

The discovery of offshore oil in the late 2000s reignited borrowing, with expectations of sustained export revenues. Public sector wages, energy sector shortfalls, and election-related spending contributed to rising obligations. When commodity prices fluctuated and revenues underperformed, repayment capacity weakened.

By the early 2020s, Ghana undertook major restructuring efforts supported by international partners. While reforms stabilized the economy, debt levels remained high by 2026, reflecting years of accumulated obligations and the difficulty of reversing entrenched spending patterns.

6. Zambia

Estimated debt-to-GDP ratio in 2026: about 115 to 120 percent.

Zambia’s debt story is inseparable from copper. Since independence in 1964, the country’s fortunes have risen and fallen with global metal prices. Borrowing accelerated during periods of high prices, particularly in the 2010s, when the government financed roads, airports, and power projects.

As copper prices softened and export revenues declined, Zambia struggled to meet repayment schedules. The country became Africa’s first pandemic-era sovereign default in 2020, marking a turning point in its debt narrative.

Subsequent negotiations with creditors and gradual restructuring provided breathing space, but by 2026, Zambia’s debt-to-GDP ratio remained elevated. The economy continues to rely on mining exports, making long-term stability highly sensitive to external market conditions.

5. Sierra Leone

Estimated debt-to-GDP ratio in 2026: about 120 to 125 percent

Sierra Leone emerged from a devastating civil war in the early 2000s with minimal infrastructure and weakened institutions. Post-conflict borrowing focused on rebuilding roads, schools, hospitals, and basic government capacity.

Progress was repeatedly disrupted by external shocks, including the Ebola outbreak and later global economic slowdowns. Mining revenues from iron ore fluctuated sharply, undermining fiscal planning and foreign exchange earnings.

By 2026, Sierra Leone’s high debt-to-GDP ratio reflects the cost of reconstruction in a small economy with limited diversification. Much of the borrowing financed essential services rather than large-scale revenue-generating assets, complicating repayment prospects.

Estimated debt-to-GDP ratio in 2026: about 130 percent

4. Egypt

Egypt’s debt accumulation is closely linked to its size and strategic role. Since the 1970s, the country has relied on external financing to support energy subsidies, food imports, and large public works. Major projects in recent years include new cities, transport corridors, and the expansion of the Suez Canal zone.

Rapid population growth has increased demand for imports and public services, while currency adjustments raised the local cost of external obligations. Although Egypt maintains access to international markets, refinancing large volumes of debt has become increasingly expensive.

By 2026, Egypt’s debt-to-GDP ratio reflects both its ambition and its vulnerability. The economy remains systemically important, but sustained high borrowing continues to shape policy choices.

3. Sudan

Estimated debt-to-GDP ratio in 2026: about 150 percent

Sudan’s debt burden is deeply rooted in decades of conflict, sanctions, and economic isolation. Following independence in 1956, political instability limited development and discouraged investment. Prolonged civil wars diverted resources toward security spending and humanitarian needs.

By the 1990s, arrears accumulated as Sudan lost access to international finance. Steps toward debt relief gained momentum in the late 2010s, with reforms aimed at clearing arrears and normalizing relations with creditors. These efforts briefly improved prospects.

However, renewed conflict in the 2020s reversed much of this progress. Infrastructure damage, displaced populations, and collapsing revenues pushed borrowing higher. By 2026, Sudan’s debt-to-GDP ratio reflects both historical arrears and the cost of ongoing instability.

2. Tunisia

Estimated debt-to-GDP ratio in 2026: about 160 percent

Tunisia’s debt escalation followed the political transition that began in 2011. While the country avoided large-scale conflict, prolonged uncertainty slowed investment and tourism, two key sources of foreign earnings.

Public borrowing increased to support subsidies, wages, and social stability during repeated political cycles. Growth lagged behind expectations, while import dependence remained high. External financing increasingly covered basic budget needs rather than expansionary projects.

By 2026, Tunisia’s debt-to-GDP ratio ranks among the highest in Africa. The country’s challenge lies in restoring growth momentum while managing a debt load built up over years of economic stagnation.

1. Eritrea

Estimated debt-to-GDP ratio in 2026: over 175 percent

Eritrea tops the list with Africa’s highest debt-to-GDP ratio in 2026. Since gaining independence in 1993, the country has operated under prolonged regional tension and international isolation. Limited access to external markets and financing channels constrained growth.

Borrowing largely supported basic state functions, security needs, and minimal infrastructure development. With a small economic base, even modest absolute borrowing translated into high debt ratios. Restricted private sector activity further limited revenue expansion.

By 2026, Eritrea’s debt burden reflects decades of isolation, low growth, and constrained economic integration. The high ratio underscores how structural factors, not just spending levels, shape national debt outcomes.

Why Debt Composition Matters

External Debt

- Common in Sudan, Mozambique, and Eritrea.

- Exposed to currency depreciation.

- Sensitive to global interest rates.

- Owed to multilaterals, bilaterals, and bondholders with limited short-term refinancing.

Domestic Debt

- Prominent in Kenya, Ghana, and Egypt.

- Lower currency risk.

- Higher refinancing and interest costs.

- Can crowd out private-sector credit and tighten domestic liquidity.

Why it matters in 2026 Many African economies now face dual exposure: rising external servicing costs alongside expanding domestic borrowing, amplifying vulnerability even where headline debt levels stabilize.

What happens next?

Debt restructuring will remain central, with several countries relying on restructuring frameworks, bilateral negotiations, and domestic debt reprofiling. While this can stabilize short-term liquidity, it does not immediately reduce debt ratios without sustained economic growth.

IMF-supported programs continue to play an important role in restoring credibility, stabilizing currencies, and unlocking concessional financing. However, they cannot fully offset weak export performance or repeated external shocks.

Growth risks remain high, including slower global growth, commodity price volatility, and climate-related disruptions. Countries with high debt have limited buffers if growth underperforms projections.

Governments with elevated debt will face difficult choices between social spending, public investment, and debt repayments, with domestic borrowing increasingly competing with private-sector credit.

What the Rankings Mean for Africa in 2026

Africa’s highest debt-to-GDP ratios in 2026 reflect the cumulative effects of structural weaknesses, external shocks, delayed reforms, and constrained growth rather than borrowing alone. For many countries, debt-financed reconstruction, social stability, and basic services rather than discretionary expansion.

The rankings highlight a widening divergence across the continent. While some economies stabilize or gradually deleverage, others remain locked in high-debt cycles where limited growth, currency pressures, and higher global interest rates reinforce fiscal stress. In 2026, Africa’s debt trajectory will be determined less by how much governments borrow and more by whether growth, exports, and institutions can finally outpace obligations.

Debt-to-GDP estimates are based on IMF Debt Sustainability Analyses, World Bank International Debt Statistics, African Development Bank data, and 2024–2025 national budget documents, with projections extended into 2026. Where figures diverge, midpoint or median estimates are used to reflect institutional consensus.

{kind=link}

Related News

Top 10 African Countries with the Lowest Public Debt in 2026

Jan 08, 2026

How Africa’s Debt Affects Inflation, Jobs and Growth

Dec 04, 2025