Table of Contents

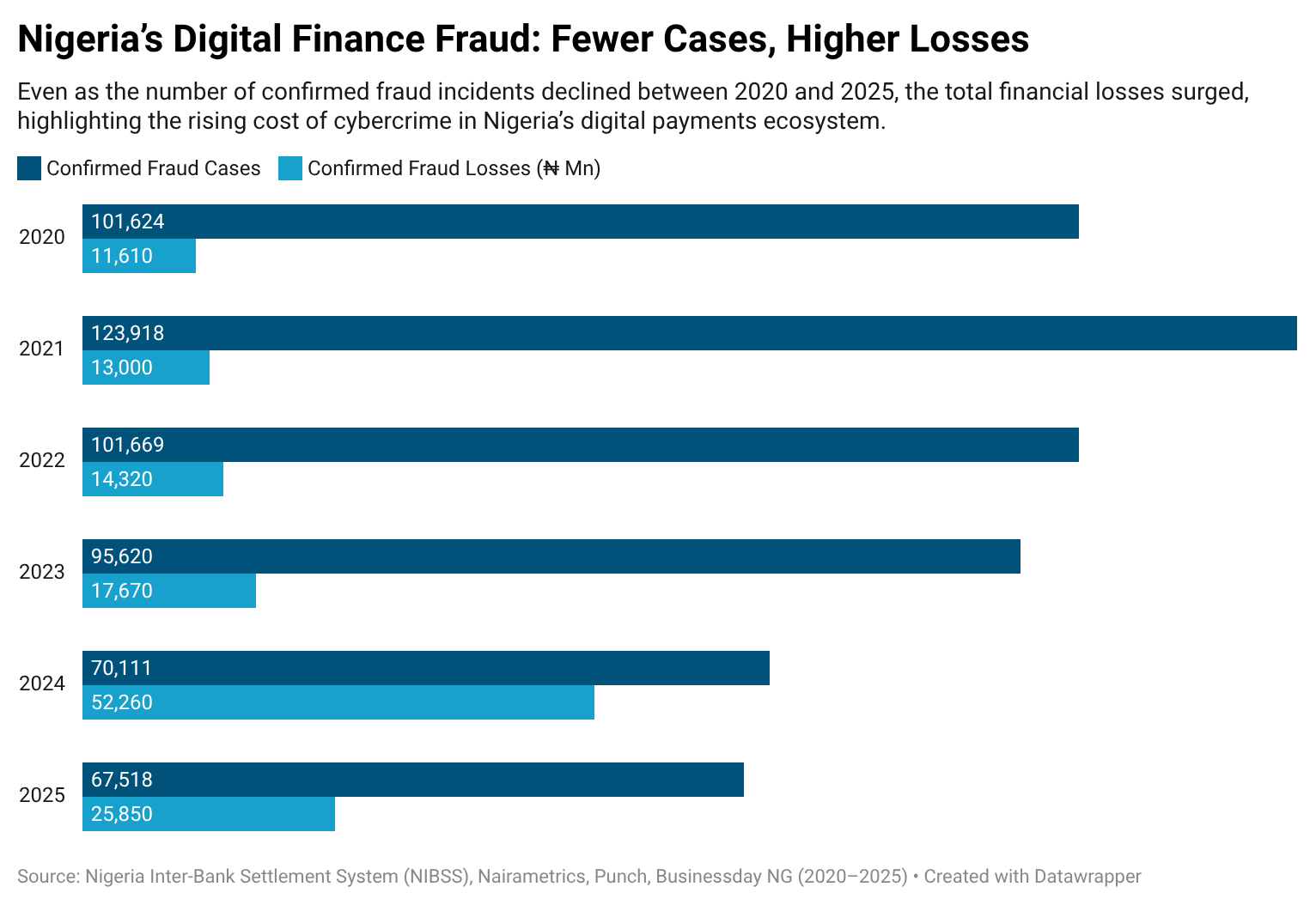

Over the past decade, Africa’s digital financial systems have expanded rapidly, creating new opportunities but also new vulnerabilities. Nowhere is this clearer than in Nigeria, where fintech platforms processed over ₦71.5 trillion ($45+ billion) in transactions in 2024. During the same period, fraud losses rose 350%, even as the total number of incidents fell. Policymakers and industry leaders have taken notice. As Dr. Chizor Malize, Managing Director of the Financial Institutions Training Centre (FITC), notes: “Cybercrime has become one of the most urgent threats facing Africa’s digital economy.”

This concern is now translating into concrete regulatory action. In Nigeria, the Central Bank introduced a cybersecurity levy requiring banks and financial institutions to contribute 0.5% of certain electronic transactions to fund national cybersecurity infrastructure and threat monitoring. In Ghana, the Bank of Ghana’s 2025 directive regulating digital credit services introduced new compliance expectations around consumer protection, operational risk management, and digital security standards for fintech platforms. Measures like these are beginning to define what cybersecurity compliance looks like in practice across African financial systems.

Yet, this urgency contrasts sharply with how financial institutions treated cybersecurity for most of the past decade. Banks and fintech startups often prioritised user growth and payment volume, treating fraud prevention as a secondary concern. Many organisations relied on basic protections like firewalls and antivirus software tools, adequate for small threats but insufficient against organised attacks on large-scale payment systems.

The risk caught up with the industry. Data from the Nigeria Inter-Bank Settlement System (NIBSS) shows that between 2020 and 2024, the number of fraud cases fell by about 31%, but total fraud losses rose by about 350%, reaching over ₦52 billion ($60+ million) in 2024.

Investigations revealed that a large share of high-value losses in early 2025 were linked to compromised credentials, insider-enabled transactions, and coordinated manipulation of digital payment flows, rather than simple scams.

Regulators across the continent have moved beyond guidance to enforcement as the scale of cyber risk became undeniable. The Interpol 2025 Africa Cyberthreat Assessment Report shows that crimes such as phishing, ransomware, and business email compromise account for a significant share of all reported offences in many African countries, even while legal and prosecution capacity remains limited. In Kenya, penalties in 2024 included fines worth $1.4 million against 11 commercial banks for failing to manage data and fraud risk, while South Africa’s Information Regulator has actively pursued firms that fail to protect customer information. These developments signal that cybersecurity is no longer optional, and institutions must demonstrate robust controls to remain in the market.

How Are Banks and Fintechs Meeting These New Cybersecurity Demands?

The shift from voluntary to mandatory cybersecurity investment has created clear market demand, but most institutions cannot meet it internally.

Across Sub-Saharan Africa, cybersecurity talent is in short supply. Industry research shows that many organisations struggle to fill cybersecurity roles. According to the World Economic Forum’s Global Cybersecurity Outlook 2026, around 70% of CEOs in Sub-Saharan Africa say their organisations lack the critical cybersecurity skills needed to meet current security objectives, one of the highest reported gaps globally. This shortage reflects the rapid growth of digital financial services across the region, limited training pipelines for specialised security professionals, and intense global competition for experienced cyber talent.

Because of this shortage, many banks and fintechs are outsourcing security functions to specialised providers. Managed Security Service Providers (MSSPs) such as Serianu and Liquid Intelligent Technologies have become key partners in this process. These firms operate Security Operations Centres (SOCs), monitor threats around the clock, respond to incidents, and assist institutions in meeting regulatory reporting requirements. Serianu has reported rising demand for cybersecurity services from banks as regulators, such as the Central Bank of Nigeria, increase oversight of fraud accountability. For many institutions, working with an MSSP is faster and more cost-effective than building an internal cybersecurity team from scratch.

Another category of solutions gaining traction is RegTech, regulatory technology focused on compliance requirements like Know Your Customer (KYC) and Anti‑Money Laundering (AML). As part of licensing conditions in Nigeria and Kenya, financial firms must implement robust identity verification systems and fraud analytics. Startups like Smile Identity, YouVerify, and Periculum provide these services as cloud‑based infrastructure. Fintech companies that cannot afford the time or expense of building these systems internally have adopted RegTech platforms as essential compliance tools.

The nature of fraud itself has also changed. Early 2025 fraud investigations showed that the largest losses, not just across Nigeria but in several reported cases in Kenya, involved insider‑enabled transactions, where compromised credentials or internal access facilitated large payments. This has created demand for a third category of security solutions: tools that monitor user behaviour, enforce access controls, and analyse internal risk dynamics. These tools are increasingly purchased alongside external threat detection systems, forming a combined security stack that regulators expect institutions to deploy.

Taken together, these trends show that banks and fintechs are not adopting cybersecurity tools casually. They are responding to enforced requirements, scarcity of internal talent, and real operational risk. This has created a layered market in which external providers capture predictable, recurring revenue.

What Does This Shift Mean for Investors Looking at African Financial Services?

For investors considering African markets, this transformation implies that cybersecurity spending is moving from an unpredictable discretionary budget item to a mandated expense with traceable demand. This is a market built on legal and regulatory requirements.

When regulators tie compliance to operating licences, institutions must spend. That converts cybersecurity into recurring, non‑discretionary demand. For investors, that kind of demand is highly valuable because it creates visibility into future revenue streams for service providers and technology vendors.

The enforcement backdrop also reduces risk. Under the old model, an institution could delay investing in security until incidents occurred or until management decided it was a priority. Now, delayed compliance risks fines, restrictions, and loss of licence. In effect, regulators have shifted security from a “nice‑to‑have” to a “must‑have,” which means spending on relevant services is predictable rather than cyclical.

This matters when allocating capital. Companies that provide security monitoring, compliance infrastructure, and internal risk analytics can expect long‑term contracts with institutions that are required to maintain those services. This provides a basis for recurring revenue, not one‑off project work.

For example, MSSPs that provide SOC services often lock in multi‑year agreements because banks and fintechs need continuous monitoring to satisfy regulatory reporting requirements. RegTech companies delivering KYC and AML infrastructure are often integrated into customer onboarding workflows, making them foundational rather than optional. Internal risk management tools, deployed to address insider threat patterns revealed in 2025 incident reports, are part of governance frameworks that regulators now expect to be documented and operational.

Investors should also pay attention to funding patterns as a signal of capital flows. The fact that cybersecurity and RegTech startups are raising significant rounds, such as Periculum’s $15 million, shows that venture capital is aligning with regulatory demand. This is not the case for every technology sector in Africa; many niches are still speculative. Cybersecurity’s linkage to compliance gives it an early‑mover advantage.

Finally, this shift reframes how investors might think about risk and valuation. Traditional concerns about African fintech regulatory uncertainty, revenue volatility, and talent gaps are mitigated in cybersecurity because the spending is tied to enforcement. Cash flows from regulated security spending can be modelled with more confidence than discretionary IT budgets.

In practical terms, that means investors can forecast revenue growth, contract renewals, and market penetration with greater certainty than in many other segments of the digital economy. Africa’s cybersecurity compliance market is an example of regulatory action creating the conditions for a predictable, durable, and measurable investment opportunity.