Table of Contents

In Summary

- Leading African sovereigns like Morocco, Côte d’Ivoire, and Benin saw Eurobond deals oversubscribed by 3 to 5 times in 2024/2025, signaling strong global investor appetite and confidence in policy credibility.

- Countries with IMF programs, restructured debt, or clear fiscal frameworks like Egypt, Ghana, and Zambia have improved access to international debt markets while managing borrowing costs effectively.

- Sovereign bond inflows support infrastructure, reform agendas, and liquidity, while providing investors with diversified yield opportunities, particularly in francophone and higher-beta African markets.

Deep Dive!!

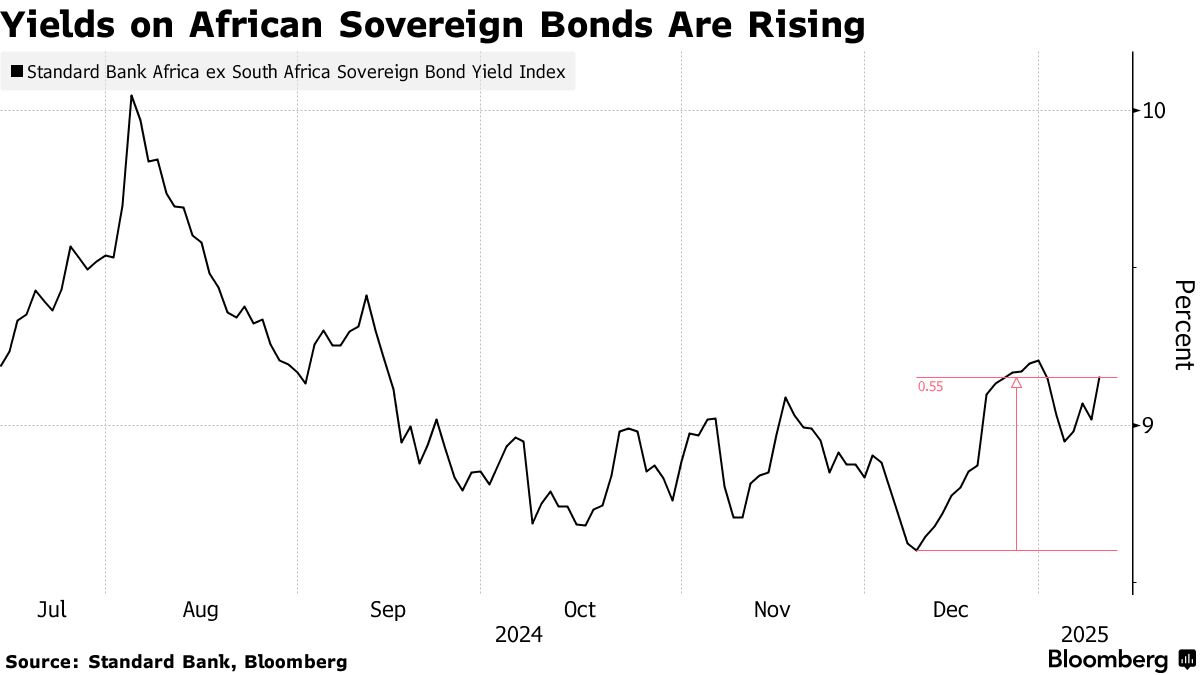

Africa’s sovereign bond market is experiencing a nuanced re-pricing as global investors re-engage with select Sub-Saharan and North African issuers, attracted by policy credibility, market access, and improving macro fundamentals despite lingering global uncertainty. The continent’s top-performing sovereign borrowers are drawing record demand, with oversubscribed Eurobond auctions, innovative liability-management operations, and robust IMF-backed reform programs restoring investor appetite after the 2022–2023 debt distress wave.

According to data from Making Finance Work for Africa (MFW4A) and market sources like Bloomberg, aggregate African sovereign issuance in the first half of 2025 has already surpassed $14 billion, up from $9.5 billion in the same period last year, underscoring the pace of re-opening in the external credit window.

This resurgence is underpinned by three converging factors. First, macroeconomic policy anchors, such as Morocco’s IMF Flexible Credit Line, Côte d’Ivoire’s growth resilience amid commodity volatility, and Benin’s disciplined issuance have created pockets of low perceived risk relative to peers. Second, investor positioning is shifting toward frontier and emerging markets offering “carry plus reform optionality,” where attractive yields are coupled with credible policy reforms or post-restructuring upside potential, as seen in Kenya, Egypt, and the turnaround stories of Ghana and Zambia. Third, the diversification of funding sources, combining Eurobond issuance, concessional loans, and local currency market development has enhanced resilience and reduced the dependency on volatile global liquidity cycles.

Yet the market remains highly differentiated. Countries with deep domestic debt markets and strong institutional frameworks, such as South Africa and Namibia, continue to attract global EM mandates even in low-growth environments, while high-beta names rely heavily on IMF programs and structural reforms to sustain investor confidence. The 2025 rankings reflect not only raw yield appeal but also the interplay of fiscal discipline, debt sustainability, and geopolitical stability. For sovereign bond investors, these top 10 African countries represent a spectrum, from stable, investment-grade-like credits to opportunistic recovery plays, where risk-adjusted returns are increasingly shaped by each government’s capacity to execute on policy commitments and leverage capital markets strategically.

Here are the top 10 most attractive African countries for sovereign bond investors in 2025.

- Zambia/Ghana

Zambia’s sovereign-credit trajectory in 2024–25 moved from crisis management to calibrated recovery after completing a landmark creditor restructuring that cleared the way for IMF support and market re-engagement. Bondholder approvals in mid-2024 closed a multilateral and private-creditor deal under the G20 Common Framework, enabling Zambia to restructure roughly $6–13 billion of external obligations and to secure follow-on financing from the IMF. Fitch and other agencies subsequently noted materially lower headline debt ratios once the haircuting and repricing were applied. This restructuring materially reduced near-term rollover risk, with the IMF and rating agencies estimate public debt falling from well above 120% of GDP in 2023 toward a substantially lower path by 2025, as Zambia shifts to a program of prudent fiscal consolidation and debt management.

Ghana’s turnaround story rests on a similarly heavy lift: comprehensive external debt negotiations combined with an IMF-supported program that has gradually restored investor confidence and unlocked critical financing. By mid-2025 Ghana’s parliament approved a $2.8 billion debt-relief agreement with official creditors, part of a broader restructuring framework that reschedules payments and materially eases near-term service burdens; the IMF has disbursed tranches under the $3 billion ECF while rating agencies (e.g., Fitch, S&P) have begun to re-rate Ghana back from default/selective-default statuses as the restructuring advances. These policy actions, plus fiscal consolidation measures and ongoing audits of arrears have created a clearer path to sustainable financing, improving the sovereign’s appeal to hard-currency bond investors seeking recovery upside rather than pure carry.

For fixed-income investors, Zambia and Ghana now represent higher-beta “turnaround” allocations with asymmetric upside if policy execution holds. Both issuers trade with elevated yields that compensate for residual execution and political risks, yet they offer potential capital appreciation as restructuring converts contingent liabilities into credible repayment schedules and as IMF program conditionality reduces tail risk. Key investor considerations remain: the pace of fiscal consolidation, transparency in arrears reconciliation, and refinancing windows for any remaining commercial debt. If governments continue to meet IMF reviews and convert agreements with official creditors into completed commercial restructurings, both Zambia and Ghana could migrate from distressed credits to higher-quality emerging-market allocations, rewarding investors willing to underwrite near-term volatility for longer-term recovery value.

- Nigeria

Nigeria’s case for 2025 rests on visible reform traction and re-opening channels to external capital. After a tentative 2024 return to international markets, officials signaled they’ll “tap a range of instruments” in 2025 to finance the budget, keeping Eurobond re-engagement on the table alongside multilateral and domestic options. Secondary performance shows the door is ajar: the Debt Management Office publishes daily Eurobond price/yield sheets, and bid-side depth has improved in 2025 versus mid-2024 stress. An interview with Finance Minister Wale Edun in January underscored investor reception, highlighting heavy oversubscription on Nigeria’s latest placement as the country rebuilds market credibility.

Macro anchors are firmer than a year ago. The IMF’s 2024 Article IV noted progress on exchange-rate unification and fuel-subsidy rollback, core to restoring FX price discovery and narrowing fiscal gaps. Inflation finally broke lower in June 2025 to 29.4% y/y (first deceleration in a year), even as the Central Bank of Nigeria pushed the policy rate up to a punishing 30% in July to consolidate disinflation and stabilize the naira. Higher oil output, at a multi-year high by mid-2025 adds external-balance breathing room, while fresh liability-management steps (including refinancing in the power sector) point to more systematic debt operations. For bond investors, the mix of tighter policy, improving oil receipts, and a functioning FX regime is the precondition for spread compression from distressed-style levels.

Risks are not trivial: inflation is still very high in absolute terms; FX liquidity is better but not yet “deep and durable”; and reform slippage would quickly re-price risk. That said, Nigeria screens attractive for carry-seekers who can stomach volatility and underwrite policy continuity. The upside scenario couples continued CBN orthodoxy and FX rule-clarity with measured external issuance, allowing the sovereign to term-out obligations while letting the local curve re-price lower as inflation trends down. In that path, Nigeria’s Eurobonds have room for both spread tightening and price gains; in the base case, investors are at least paid to wait.

- Namibia

Namibia has steadily built a reputation as one of Sub-Saharan Africa’s most disciplined sovereign issuers, a perception reinforced by its upcoming $750 million Eurobond maturity in October 2025. The government has pre-funded the bulk of this obligation through a well-structured sinking fund, leaving only a modest portion to be refinanced, thereby limiting rollover risk and removing a key concern for bondholders. This proactive approach to liability management has been noted by international rating agencies, which view Namibia’s fiscal prudence as a positive differentiator in a volatile African credit landscape. The IMF has not had to provide an emergency program, underscoring the country’s self-sufficiency in managing external obligations.

The country’s macroeconomic backdrop is strengthening, supported by significant offshore oil and gas discoveries in the Orange Basin. These findings, potentially among the largest in Africa over the past decade have driven a surge in foreign investor interest, not only in Namibia’s extractive sector but also in its sovereign debt. While first oil is still a few years away, preliminary development agreements and capital inflows from major energy companies have begun improving the balance of payments outlook and enhancing medium-term fiscal prospects. Real GDP growth, which averaged around 3.7% in 2024, is projected to edge higher in 2025 as mining and construction activity accelerates. Inflation remains moderate by regional standards, hovering around 5–6%, aided by a currency peg to the South African rand, which anchors monetary stability.

For fixed-income investors, Namibian Eurobonds offer a solid carry trade profile: relatively high yields compared to similar-rated peers, yet with lower default risk thanks to conservative fiscal management and credible policy execution. The bond curve remains well-behaved, reflecting confidence in the government’s redemption plan for 2025 and optimism over medium-term hydrocarbon revenues. Furthermore, Namibia’s integration into the Southern African Customs Union (SACU) provides steady customs revenue inflows, further reinforcing fiscal buffers. For investors seeking stable African exposure without the headline risk of higher-beta credits, Namibia represents a compelling “steady hands” allocation in 2025.

- Kenya

Kenya reinforced its market credibility in 2024 with a $1.5 billion Eurobond issuance that was strategically timed to facilitate the buyback of its $2 billion 2024 maturity, avoiding refinancing stress and proving sustained access to capital markets. The deal attracted strong interest despite global monetary tightening, with orders exceeding expectations and pricing inside initial guidance. This operation was paired with concessional financing from multilateral partners, enabling the Treasury to smooth its maturity profile and reduce rollover risk. The International Monetary Fund (IMF), under its Extended Fund Facility (EFF) and Extended Credit Facility (ECF), has consistently flagged Kenya’s proactive debt management as a credit-positive, noting improved fiscal transparency and greater alignment with medium-term debt sustainability targets.

Macroeconomic momentum underpins the credit’s appeal. GDP growth in 2024 was estimated at 5.4% and is projected to remain above 5% in 2025, driven by robust agricultural recovery, expanding service exports (notably ICT and tourism), and sustained infrastructure investment. Inflation eased from over 9% in early 2023 to the 6–7% range in mid-2025, aided by a relatively stable exchange rate and targeted food supply interventions. The IMF’s most recent Kenya program review approved disbursements totaling over $600 million, strengthening reserves and providing a policy anchor for ongoing reforms in revenue mobilization, energy subsidy rationalization, and SOE governance. This framework has reassured investors that Nairobi is committed to fiscal consolidation without undermining growth prospects.

From an investor perspective, Kenya’s sovereign spreads remain among the most attractive in Sub-Saharan Africa for carry trade strategies, offering high yields relative to its improving macro fundamentals. The Eurobond curve has compressed since the 2024 buyback but still prices in reform execution risk, creating potential for capital gains if fiscal consolidation accelerates. Participation in the African Continental Free Trade Area (AfCFTA) and ongoing port and rail upgrades position Kenya as a key logistics hub for East Africa, enhancing long-term external sector resilience. For investors with tolerance for moderate credit volatility, Kenya presents a compelling mix of high yield, proven market access, and reform-driven upside.

- Egypt

Egypt continues to present an appealing, albeit high-beta, opportunity for sovereign bond investors seeking upside amid credible policy anchors. In March 2024, the country secured an expanded $8 billion Extended Fund Facility (EFF) with the IMF, building on an earlier $3 billion program. By early 2025, following the fourth review, Egypt unlocked $1.2 billion in disbursements and gained access to approximately $1.3 billion under the Resilience and Sustainability Facility (RSF), effectively boosting its external financing space.

These arrangements, paired with a flexible exchange rate regime and aggressive monetary tightening, helped arrest inflation and stabilize macroeconomic expectations. Adding to the confidence-building measures, Egypt struck a landmark $35 billion investment agreement with Abu Dhabi’s ADQ to develop Ras El Hekma, its largest-ever FDI deal. In tandem with grants and loans from the EU, World Bank, and Gulf partners, the package helped close a deep financing gap and bolster foreign exchange reserves.

The transformation of a portion of ADQ’s deposits into EGP-denominated funding and efforts to clear FX backlogs have reinforced Egypt’s reserve buffers and reduced short-term rollover risk. However, challenges remain. Inflation, though improved, remains elevated, hovering around 13–17% in mid-2025, down from over 30% in early 2024.

Fiscal consolidation is ongoing, with divestments from state entities earmarked to support debt reduction and improve debt dynamics. Egypt’s reliance on reform execution and regional stability underscores the credit’s vulnerability to external shocks. Nonetheless, for investors with an appetite for higher yield and credible reform trajectory, Egypt offers asymmetric upside supported by IMF backstops and transformational FDI. You can find more about FDI in our article titled ‘Top 10 Development Finance Institutions (DFI) in Africa 2025’

- South Africa

South Africa remains a cornerstone for sovereign bond investors navigating African markets, thanks to its deepest and most liquid onshore bond market in Sub-Saharan Africa. The country issues a robust range of maturities, with benchmark bonds spanning 2 to 30 years, that are actively traded by local and global institutional players. Even amid recent growth headwinds (e.g., sub-3% real GDP growth), investors continue to value SA for its rule-of-law strength, transparent central bank policy via the SARB, and developed pension-fund ecosystem. These structural advantages make South Africa particularly appealing for local-currency (LCY) mandates, where predictability, liquidity, and legal enforceability are critical.

While global appetite for emerging-market external debt (e.g., Eurobonds) has been volatile, South Africa’s reliable LCY infrastructure serves as an effective cushion, enabling investors to maintain or increase exposure without excessive currency or rollover risk. Its inclusion in key indexes (e.g., JPMorgan GBI-EM, Bloomberg Barclays EM Local) further ensures steady passive inflows, even during lean risk-on periods. The country’s ability to host regular, well-received auctions, often oversubscribed, signals consistent investor confidence. For sovereign bond portfolios structured to hold onshore assets, South Africa remains a key core allocation in Africa, balancing yield pickup with policy credibility.

Looking ahead to 2025, South Africa may not offer the highest carry compared to frontier issuers, but it delivers a distinct blend of liquidity, transparency, and strategic diversification that many EM investors prize. While domestic fiscal pressures (electricity constraints, debt servicing) are real, numerous institutional investors see SA as a stabilizing anchor for continent-wide exposure. As African EM bond markets evolve, South Africa’s well-established infrastructure and legal framework ensure it continues to stand out as a comparatively low-tail-risk sovereign, making it a risk-adjusted allocation of choice, especially for long-duration and local-currency strategies.

- Senegal

Senegal returned to the sovereign Eurobond market in June 2024, issuing $750 million in two tranches maturing in 2031 at a coupon of 7.75%, led by JPMorgan. Despite concerns about political transition, the offering was seen as a vote of confidence in new leadership and marked Senegal as a credible issuer amid renewed access for Sub-Saharan African sovereigns.

Since then, Senegal has demonstrated strong investor appetite in its domestic and regional funding channels. In the first half of 2025, it issued CFA 364 billion (~$644 million) in an oversubscribed domestic bond offering, exceeding the target by over 21%, despite an S&P downgrade to B- amid fiscal concerns. Meanwhile, it made a regional financing mark with a record CFA 405 billion (~$717 million) multi-tranche issuance on the BRVM, showcasing both depth and investor trust in WAEMU markets.

However, Senegal's impressive issuance performance belies underlying fiscal vulnerabilities. The IMF suspended its $1.8 billion support program after uncovering $7 billion of previously undisclosed liabilities, pushing the debt-to-GDP ratio near 120%. Dollar sovereign bonds consequently underperformed, falling 7.3% compared to regional peers. Nonetheless, the government's pivot to domestic markets, despite ratings pressure, indicates adaptability and reinforces its appeal as a “core francophone” credit with diversified funding strategies.

- Benin

Benin entered the global bond market with a strong debut; in mid-February 2024, the country raised $750 million via a 14-year US dollar Eurobond, priced around 7.96% (equivalent euro coupon ~6.5% after a swap). Remarkably, the order book attracted ~$5 billion in demand, making it more than 6× oversubscribed, signaling serious investor interest despite Benin’s small size.

Less than a year later, in January 2025, Benin returned with another $500 million bond issuance that drew $3.5 billion in demand, again massively oversubscribed. The offering included a €€1 billion funding package (Eurobond + loan), supporting liability management and refinancing.

Benin’s financial credibility also gained external validation. In April 2024, Standard & Poor’s upgraded the sovereign’s credit rating from B+ to BB-, citing improved fiscal discipline and policy frameworks, and retained a stable outlook. Fitch maintained B+, reinforcing confidence in the country’s debt management. Additionally, Benin ranked first among Francophone African countries in the 2023 Open Budget Survey, scoring 79/100, a strong signal of growing transparency and institutional maturity.

Benin’s issuance strategy emphasizes longer-dated funding to extend its maturity profile and minimize rollover risks, key in a WAEMU context where short-term regional debt often dominates. It also structured deals tying proceeds to SDG-focused investments, boosting appeal with global investors seeking ESG-aligned sovereigns. Moreover, this approach, in conjunction with support from IMF resilience instruments, signals prudence and forward-looking risk management. For sovereign bond investors, Benin offers a compelling blend of carry potential, growing fiscal credibility, and attractive market access.

Benin is a standout frontier issuer: its strong debut and repeat bids, transparent governance, and strategic structuring elevate it to a “policy-credible small-cap” role in African sovereign credit. For investors targeting emerging African hard-currency debt with reform narratives and ESG framing, Benin offers a rare and compelling opportunity.

- Côte d’Ivoire

In January 2024, Côte d’Ivoire returned to the international sovereign debt market after a two-year hiatus, launching a $2.6 billion dual-tranche Eurobond with maturities of 9 and 13 years. The issuance was met with overwhelming demand, orders exceeded $8 billion from more than 400 global investors, marking the largest bond offer ever from a West African sovereign. That level of interest reflects a significant resurgence in investor confidence across Sub-Saharan African credit markets.

Côte d’Ivoire deployed much of the raised funds toward liability management, including refinancing upcoming bond maturities and commercial loans, actions designed to smooth its amortization schedule and reduce rollover risks. Additionally, in a strategic move, the country issued a CFA franc–denominated tranche in international markets, the first African sovereign to do so, diversifying its currency profile and reinforcing its capital market footprint. S&P highlighted these actions as drivers of improved debt dynamics and solid institutional credibility.

Despite challenges from adverse weather that caused a 23% decline in cocoa output in 2023, Côte d’Ivoire benefitted from sharply increased cocoa prices, expected to raise cocoa export revenues from 7% of GDP in 2023 to about 11% in 2025, further bolstering external balances. Real GDP growth has held steady at 6.2% in 2023, and projections for 2025 are even stronger, with forecasts ranging up to 6.7%, supported by infrastructure investment, hydrocarbon and mining export gains, and a still-resilient service sector.

Côte d’Ivoire’s sovereign bond profile in 2025 stands out with its successful Eurobond issuance, smart use of proceeds to manage debt, evolving funding strategies including local currency issuance, and solid macroeconomic resilience, even amid agricultural shocks. These traits place it among the most attractive and strategically credible African sovereign issuers for bond investors.

- Morocco

Morocco’s sovereign bond market performance in 2025 has cemented its position as Africa’s most attractive destination for fixed-income investors. In March, the country successfully issued a $2.5 billion dual-tranche Eurobond (10- and 30-year maturities), attracting an impressive $7 billion in orders, nearly three times the offer size. This deal came just days after Morocco secured an IMF Flexible Credit Line (FCL), a rare instrument granted only to countries with strong macroeconomic fundamentals, prudent fiscal policy, and robust external buffers. The FCL acts as a powerful market signal, reducing perceived sovereign risk and effectively lowering borrowing costs. These developments underscore investor confidence not only in Morocco’s credit profile but also in its policy consistency, which has helped the country maintain stability despite global market volatility.

The appeal is also rooted in Morocco’s economic diversification and fiscal reforms. The government has been proactive in strengthening its debt management strategy, extending maturities, and securing financing at favorable rates. With a growing export base, particularly in automotive manufacturing, renewable energy, and phosphates, Morocco benefits from steady foreign exchange inflows that improve debt servicing capacity. The country’s investment-grade rating from major agencies further differentiates it from many sub-Saharan peers, positioning it as a “core holding” for global emerging market (EM) bond portfolios. Moreover, fiscal consolidation efforts, coupled with targeted infrastructure investments, align with Morocco’s long-term vision to deepen domestic capital markets and attract sustained foreign investment.

From a market access perspective, Morocco operates in a different risk league compared to most African issuers. Its Eurobond oversubscription is not merely a sign of temporary yield hunting but reflects a strong structural investor base that includes global asset managers, sovereign wealth funds, and long-term pension funds. This depth of investor confidence grants Morocco greater flexibility in timing future issuances and managing refinancing risks. For sovereign bond investors seeking a balance of yield, liquidity, and stability, Morocco represents a rare African issuer that offers both attractive carry and credible downside protection, a combination reinforced by its IMF-backed safety net and disciplined fiscal policy.

{kind=link}