In Summary

- In the 2023/2024 cultivation season, Africa produced an estimated 3.151 million metric tons of cocoa, accounting for approximately 70% of global production.

- Industry sources are predicting a 10% drop in cocoa production for the 2025/26 season in the four main producing countries: Ivory Coast, Ghana, Nigeria, and Cameroon, according to Tridge.

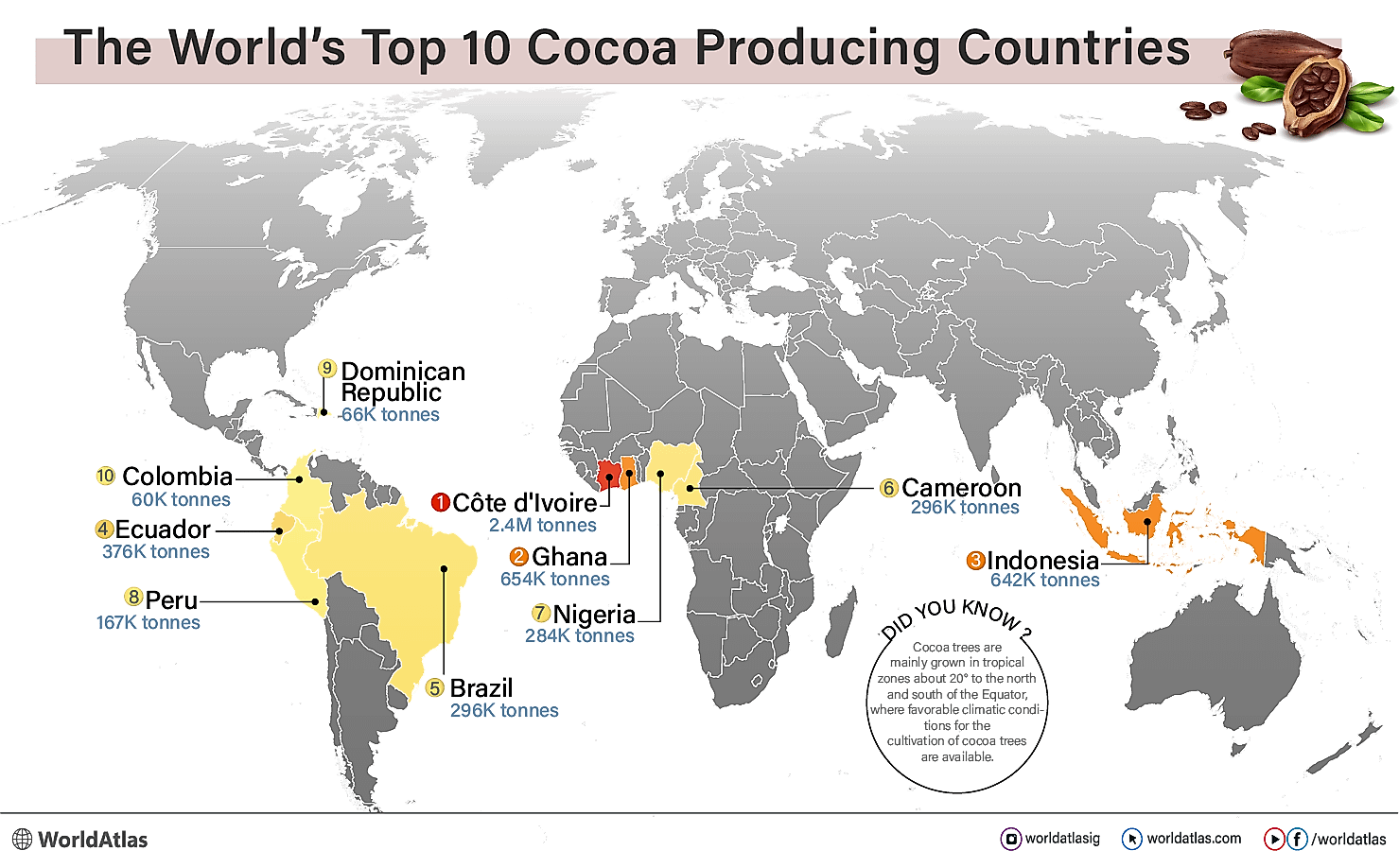

- Côte d'Ivoire, Africa’s largest producer of Cocoa produces around 2.2 million metric tons annually, according to Intelpoint.

Deep Dive!!

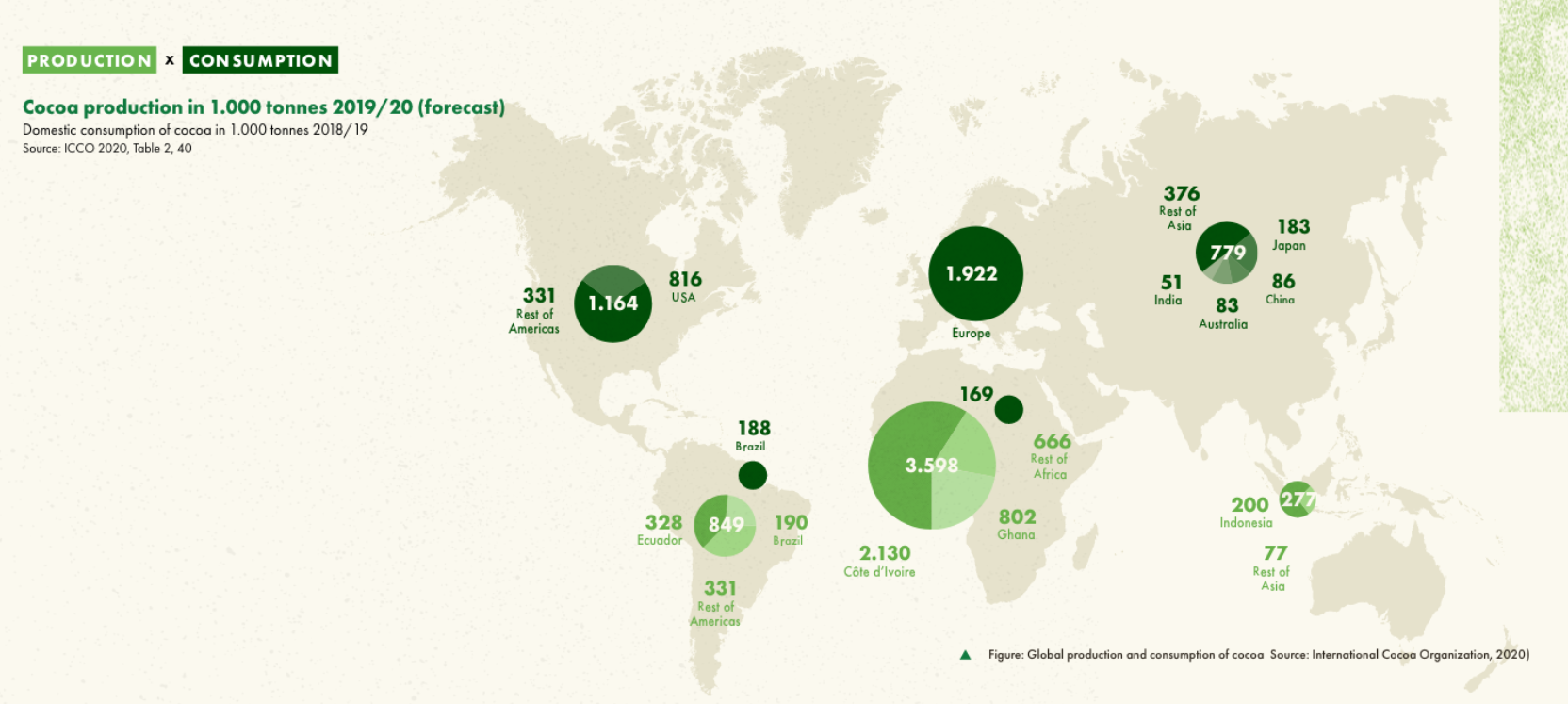

Over the years, cocoa has remained one of Africa’s most valuable agricultural commodities, serving as both a cornerstone of rural livelihoods and a major contributor to national export earnings. As of 2023, African countries collectively accounted for over 70 % of global cocoa output, with Côte d’Ivoire, Ghana, Cameroon, and Nigeria alone supplying more than two-thirds of the world’s beans. Côte d’Ivoire maintained its position as the undisputed leader, producing approximately 2.38 million tonnes (around 42 % of global supply), while Ghana followed with an estimated 654,000 tonnes despite weather and disease-related setbacks. This dominance is not merely a matter of volume; it reflects a deeply entrenched agricultural heritage, extensive smallholder participation, and trade linkages that reach every major chocolate-producing region in the world.

The scale and importance of cocoa to African economies are underscored by its role in foreign exchange generation and non-oil export diversification. In Nigeria, for example, cocoa-bean exports in 2024 were valued at roughly ₦2.7 trillion (about $1.7 billion), bolstering trade balances amid volatile oil revenues. Ghana’s cocoa sector, employing nearly 800,000 farm families, consistently delivers over $2 billion in foreign currency earnings in normal production years, while Cameroon’s industry, responsible for around 296,000 tonnes annually, has already georeferenced 80 % of its farms to comply with the EU’s deforestation-free regulations. Smaller producers such as Uganda, Madagascar, Guinea, and Liberia, though modest in output, are increasingly leveraging niche quality, specialty certifications, and rising global prices to carve out competitive market positions.

This economic weight is magnified by cocoa’s rural development impact. Across the continent, the sector provides direct income for millions of smallholder farmers, stimulates local commerce through the purchase of goods and services, and supports employment in transport, warehousing, and processing. In countries like Sierra Leone and Guinea, cocoa constitutes one of the top five export earners, sustaining household cash flow in regions where alternative income sources are limited. With international prices reaching multi-decade highs in 2024–2025, farm-gate incomes have risen sharply, enabling smallholders to reinvest in orchard rehabilitation, improved fermentation and drying techniques, and compliance with new market traceability standards.

Yet Africa’s cocoa powerhouse status faces mounting challenges that demand strategic responses. Climate variability, aging tree stocks, soil degradation, and plant diseases such as swollen-shoot threaten long-term yields. Moreover, the European Union’s new Deforestation Regulation (EUDR), set to take full effect in 2025, will require robust farm-level traceability, posing compliance risks for producers lacking infrastructure or formalized supply chains. At the same time, opportunities abound: scaling domestic grinding capacity to capture more value-added, investing in disease-resistant hybrids, and leveraging technology for real-time farm mapping could secure Africa’s position as the engine of the global cocoa trade. In this article, we examine the continent’s top ten cocoa producers, ranked from 10 to 1, not only in terms of production data but also their economic impact, challenges, and future trajectories in a rapidly evolving global commodity landscape.

10. Sierra Leone

In 2023, Sierra Leone’s cocoa sector produced an estimated 18,000 tonnes, cementing its role as one of the country’s most important agricultural industries despite its modest global standing. Cocoa beans ranked among the nation’s top five merchandise exports, generating approximately $50 million in foreign exchange earnings, with the EU, especially the Netherlands absorbing the majority of shipments. This export profile underscores the commodity’s disproportionate economic importance relative to Sierra Leone’s small GDP and narrow export base. For a country still rebuilding from years of conflict and economic fragility, cocoa provides a rare and stable link to international markets, offering both fiscal and developmental benefits that outweigh its sheer production volume.

Production trends, however, have been inconsistent, shaped by structural and agronomic constraints. Aging tree stocks, low-yield planting materials, weak input supply chains, and poor rural road infrastructure have historically kept yields below potential. These challenges are compounded by fluctuating weather patterns and inadequate quality control systems, which limit Sierra Leone’s competitiveness in premium markets. Nonetheless, the record-breaking surge in global cocoa prices since 2024 has reinvigorated farmer engagement in orchard rehabilitation, pruning, and improved husbandry practices. Higher farm-gate prices have created a window of opportunity for sector reform, incentivizing both smallholders and cooperatives to adopt better production and post-harvest methods in anticipation of long-term gains.

At the community level, cocoa serves as a critical income anchor for tens of thousands of smallholder households in the Eastern and Southern Provinces, where cash-crop alternatives are limited. The value chain remains largely informal, leaving many farmers without structured market access, formal financing, or price transparency. This informality also poses compliance risks under the European Union’s deforestation-free regulation (EUDR), which will soon require verified traceability for all cocoa imports into the EU. Addressing these bottlenecks through farmer aggregation centers, cooperative-led certification programs, targeted rural infrastructure investments, and accessible warehouse financing could materially raise farmer margins, safeguard export market access, and stabilize national foreign exchange receipts. Sierra Leone’s case reflects a broader African truth: even relatively small cocoa producers can unlock significant economic and developmental impact if structural weaknesses are addressed and global market opportunities are strategically harnessed.

9. Liberia

Liberia’s cocoa industry, while small by global standards, occupies a strategically important position within West Africa’s cocoa belt. In 2023, national production stood at roughly 20,000 tonnes, according to FAO estimates, with cocoa-bean exports valued at approximately $55 million. The bulk of these shipments went to the Netherlands and Indonesia, linking Liberia firmly to both European and Asian processing hubs. Geographically, many of Liberia’s cocoa-growing areas lie along the Ivorian border, a location that facilitates trade integration but also enables informal cross-border flows. Such leakages, while sometimes offering farmers higher immediate returns, can distort official trade data, undermine export tax collection, and complicate efforts to certify supply chains under emerging international sustainability regulations.

The recent surge in global cocoa prices has offered Liberian farmers a rare profitability boost, making orchard rehabilitation and improved husbandry practices more financially attractive. Yet, sustained gains will depend on tackling structural weaknesses in land-use governance, traceability systems, and post-harvest quality management. Deforestation risks linked to agricultural expansion remain a pressing concern, particularly as the European Union’s deforestation-free regulation (EUDR) moves toward full enforcement in 2025. Meeting these standards will require coordinated investment in farmer services, such as access to improved seedlings, pruning programs, and fermentation/drying infrastructure, alongside better logistics and aggregation points to reduce transaction costs. These measures would enable Liberia to channel more of its output into compliant, premium-paying markets, significantly increasing value capture per tonne.

From a macroeconomic perspective, cocoa accounts for only a small fraction of Liberia’s GDP, yet it represents a meaningful share of non-mineral export earnings and a vital source of rural income. With an economy heavily reliant on mining, shipping, and a narrow range of agricultural commodities, each incremental gain in compliant cocoa exports contributes directly to foreign exchange diversification and fiscal stability. In remote farming regions, cocoa income supports household consumption, education, and community investment, anchoring local economies where alternative cash crops are scarce. As such, the sector’s growth potential is not merely an agricultural concern but a strategic economic imperative, offering Liberia a pathway to broaden its export base, strengthen rural livelihoods, and position itself more competitively within the global cocoa trade.

8. Madagascar

Madagascar’s cocoa sector, though modest in scale, occupies a unique and prestigious position in the global market. Producing roughly 20,000 tonnes in 2023, the country’s exports were valued at around $37.5 million, with buyers willing to pay significant premiums for its reputation as a fine-flavor origin. Malagasy cocoa, often marketed alongside its globally renowned vanilla, commands higher-than-average prices thanks to terroir-specific branding, meticulous fermentation processes, and widespread adoption of organic and ethical certifications. The global supply squeeze in 2024 further amplified these premiums, allowing farmers and exporters to capitalize on scarcity while reinforcing the island’s positioning in high-end confectionery and specialty chocolate markets.

Production is heavily concentrated in the Sambirano Valley in the northwest, where climatic conditions, soil profiles, and established processing traditions support the production of complex, aromatic beans. In this region, smallholders benefit from direct relationships with specialty buyers and NGOs that provide post-harvest training, quality control services, and access to premium markets. However, Madagascar’s cocoa sector faces inherent constraints in scale such as, aging orchards limit productivity growth, while climate variability, particularly erratic rainfall patterns threaten consistent yields and bean quality. Given these challenges, the strategic path forward lies not in mass production but in deepening the country’s specialization in high-value niches, where quality can offset limited volume and preserve farmer profitability.

Economically, cocoa remains a niche but important contributor to Madagascar’s agricultural export portfolio, complementing dominant earners like vanilla and cloves. Its role as a diversification crop is particularly valuable in insulating the economy from the volatility of vanilla prices, which have historically swung wildly due to global supply imbalances. By expanding onshore fine-flavor processing, such as couverture chocolate, cocoa liquor, and artisanal bars, Madagascar could capture greater value within its borders, create skilled jobs, and enhance brand recognition in global premium markets. Strengthening infrastructure for quality certification, expanding cooperative-led marketing, and investing in climate-resilient cocoa varieties would further secure the sector’s long-term competitiveness while maintaining the island’s reputation as a source of some of the world’s most distinctive cocoa.

7. Guinea

Guinea’s cocoa sector has experienced a notable upswing in recent years, with 2023 production estimated at roughly 23,000 tonnes according to FAO data. What stands out, however, is the disproportionate value of its cocoa exports, approximately $216 million in 2023 pointing to both strong trade growth and the likelihood of re-export activity through Guinean corridors. The country’s primary buyers include major processing and trading hubs such as the Netherlands, Indonesia, and Malaysia, indicating that Guinean cocoa is firmly integrated into the global supply chain. This trade profile suggests that while domestic production is expanding, Guinea’s geographic location, bordering major cocoa producers like Côte d’Ivoire and Liberia enables it to serve as a channel for cross-border bean flows, whether formal or informal.

On the ground, the sector is characterized by rapid smallholder entry, particularly as high global prices since 2024 have made cocoa an attractive cash crop for rural farmers. However, this expansion has been accompanied by mixed quality control standards and porous borders, which create challenges in maintaining origin integrity. The surge in exports has also placed a spotlight on compliance with the European Union’s deforestation-free regulation (EUDR), which will soon require precise traceability from farm to port. Without robust mapping, monitoring, and certification systems, Guinea risks losing access to its most lucrative markets. Elevating sector governance through centralized fermentation hubs, coordinated quality assurance, and farmer cooperatives equipped with digital traceability tools will be essential to ensure that current gains are sustainable and compliant.

From an economic standpoint, cocoa is emerging as an important non-mineral foreign exchange earner for Guinea, complementing dominant export sectors like bauxite and gold. Diversifying the export base in this way enhances resilience against commodity price volatility in the mining sector, while generating rural incomes in regions with few alternative cash crops. A strategic focus on raising unit values through quality upgrades, better fermentation, and access to premium certification could significantly boost export revenues without requiring vast increases in land under cultivation. By investing in skills development, supply chain formalization, and market access infrastructure, Guinea has the potential to position its cocoa sector not merely as an opportunistic beneficiary of high prices, but as a stable, value-driven pillar of the national economy.

6. Uganda

Uganda’s cocoa sector has gained significant traction in recent years, moving from a modest agricultural subsector to a visible contributor to national export performance. In 2023, production stood at approximately 35,000 tonnes, but the real story lies in the recent surge in export volumes and revenues. Bank of Uganda data show that from March 2024 to February 2025, cocoa exports totaled around 56,000 tonnes, with March 2025 earnings alone increasing by an impressive 72% year-on-year. This momentum reflects both higher global prices and expanding production capacity, positioning cocoa as an increasingly important pillar in Uganda’s non-coffee export portfolio and a valuable complement to traditional forex earners like gold.

Production is dominated by smallholder farmers in western districts such as Bundibugyo, where favorable agro-climatic conditions and improved infrastructure, particularly rural roads have reduced transport costs and improved market access. The influx of private-sector buyers has further stimulated competition, raising farm-gate prices and incentivizing investment in orchard rehabilitation, pruning, and improved husbandry practices. However, sustaining these gains requires addressing vulnerabilities in seed quality, pest and disease surveillance, and post-harvest handling. Without stronger quality control systems, Uganda risks losing the competitive edge needed to access premium-paying markets, especially under tightening European Union traceability and deforestation-free requirements.

Economically, cocoa offers Uganda a strategic avenue for export diversification at a time when dependence on coffee and gold leaves the country exposed to commodity price volatility. The sector’s growth potential extends beyond raw-bean exports; investments in domestic value addition, such as cocoa liquor, butter, and powder production could capture more revenue domestically and create rural employment. To fully capitalize on current market conditions, the government and development finance institutions (DFIs) can play a catalytic role by scaling seedling distribution programs, expanding farmer training on fermentation and drying, and establishing cooperative-led certification pathways. These measures would not only safeguard Uganda’s access to high-value EU markets but also position the country as a competitive, sustainable, and premium-origin supplier in the global cocoa trade.

5. Democratic Republic of the Congo (DRC)

The Democratic Republic of the Congo (DRC) produced an estimated 35,000 tonnes of cocoa in 2023, according to FAO data, with production concentrated in the eastern provinces of North Kivu and Ituri. While this volume places the country in the mid-tier of African producers, it significantly understates the sector’s potential. The region’s fertile soils and favorable climatic conditions could support much higher yields if systemic barriers were addressed. Improved security, rehabilitation of feeder roads, and a stronger presence of reliable buyers would allow more beans to enter formal markets, increasing the marketed surplus and boosting export earnings. The country’s proximity to key trade corridors in East Africa also offers opportunities for greater regional integration in the cocoa trade.

The sector’s primary challenges lie in logistics and quality control. When global cocoa prices are high, as they have been since 2024, farmers are more willing to absorb high transport costs and security risks to get beans to market. However, when prices normalize, poor road access, limited storage facilities, and insecurity in producing areas severely erode farm-gate prices and reduce volumes sold. Quality consistency is also an issue, with insufficient access to drying equipment, fermentation facilities, and grading standards limiting competitiveness in premium markets. Targeted investments in farmer aggregation centers, solar-powered drying systems, and community-led traceability programs could significantly enhance both bean quality and the share of final prices that reaches producers, creating a more resilient value chain.

From a macroeconomic perspective, cocoa’s national significance is modest compared to the DRC’s dominant copper and cobalt exports, which drive most foreign exchange earnings. However, regionally, particularly in the east, cocoa plays an outsized role as a source of cash income for smallholder households. Beyond its economic value, cocoa is considered a “peace-dividend” crop: its cultivation and trade provide rural communities with legal, livelihood-sustaining alternatives to illicit or conflict-related activities. Stabilizing the eastern cocoa corridor, professionalizing buying practices, and strengthening market infrastructure could help translate the current price boom into long-term rural development gains, while positioning the DRC as an emerging sustainable supplier in the African cocoa landscape.

4. Nigeria

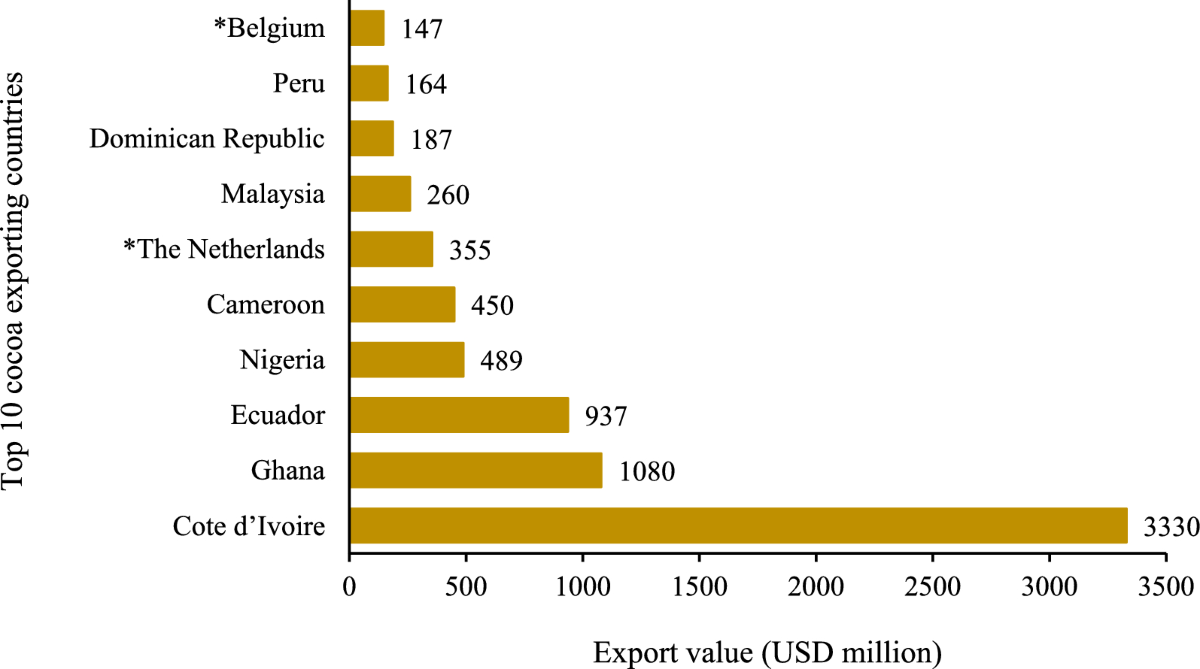

Nigeria’s cocoa sector has re-emerged as a key driver of non-oil export growth, with 2023 production estimated at 284,000 tonnes. Official trade statistics show cocoa-bean exports valued at $670 million that year, while naira-denominated export earnings surged to approximately ₦2.7 trillion (about $1.7 billion) in 2024. This remarkable increase was fueled by both record-high global cocoa prices and the currency depreciation, which boosted the local value of foreign earnings. As oil revenues came under pressure from fluctuating global markets and domestic production challenges, cocoa has stepped into the spotlight as a flagship commodity for Nigeria’s diversification strategy, providing a stable and competitive source of foreign exchange.

The production base is anchored in states such as Ondo, Cross River, and Edo, where farmers are actively replanting and rehabilitating farms after years of underinvestment. However, the sector continues to grapple with structural issues; most notably, an aging tree population and limited access to agricultural extension services. These constraints keep yields below potential and quality inconsistent. Yet, there is substantial opportunity to move beyond raw-bean exports by scaling up domestic processing into higher-value products such as cocoa butter, liquor, and cake. Expanding fermentation standards, strengthening post-harvest handling, and promoting quality certifications could enable Nigeria to capture more value onshore, reduce dependence on volatile global commodity pricing, and position itself as a reliable supplier to both premium and industrial chocolate markets.

At the macroeconomic level, cocoa has played a pivotal role in widening Nigeria’s trade surplus in early 2025 and in driving the broader surge in agricultural exports. To ensure these gains are structural rather than cyclical, targeted policies are needed, including a credible nationwide seed and farm rehabilitation program, improved farmer access to affordable finance, and export-credit facilities for processors seeking to scale operations. By combining productivity improvements with value addition, Nigeria can transform cocoa from a price-driven windfall into a resilient growth engine, strengthening rural livelihoods, boosting foreign exchange stability, and reinforcing the country’s position as one of Africa’s most important cocoa producers.

3. Cameroon

Cameroon stands as one of Africa’s largest cocoa producers, with 2023 output estimated at approximately 296,000 tonnes. Official trade data indicate that about 180,000 tonnes of raw beans were exported that year, generating close to CFA 360 billion in foreign exchange earnings. The 2024 season brought a further boost to farmer incomes as global cocoa prices surged, partly due to supply shortfalls in neighboring countries like Côte d’Ivoire and Ghana. This price environment allowed Cameroonian farmers to capture significantly higher margins, highlighting the country’s strategic position in the regional and global cocoa market. With cocoa accounting for a substantial share of agricultural export revenues, the sector remains a cornerstone of Cameroon’s trade profile.

A defining feature of Cameroon’s recent cocoa policy success is its progress in meeting the European Union’s deforestation-free regulation (EUDR) requirements. Around 80% of Cameroonian cocoa farms are now georeferenced, enabling traceability across most of the supply chain. This is critical given that approximately 80% of Cameroon’s cocoa exports are destined for EU markets. Such compliance not only safeguards market access but also positions the country to secure premiums in sustainability-conscious buyer segments. Moving forward, sector priorities include large-scale farm rehabilitation to replace aging trees, stronger phytosanitary controls to combat pests and diseases, and further improvements in post-harvest quality, especially fermentation and drying, to compete effectively in premium markets.

Economically, cocoa is among Cameroon’s top agricultural exports and a vital source of rural income, particularly in the Centre, South, and Southwest regions. The benefits of the 2024/25 price boom have been felt well beyond the farm gate, with higher incomes filtering directly into household consumption, local commerce, and community investments. These gains have helped cushion rural economies from broader macroeconomic pressures, including inflation and currency volatility. By consolidating its traceability achievements and investing in productivity and quality upgrades, Cameroon can not only retain its EU market share but also expand its role in value-added processing, thereby reinforcing the sector’s contribution to both national revenue and rural development.

2. Ghana

Ghana, the world’s second-largest cocoa producer, recorded an estimated 654,000 tonnes of output in 2023, but the 2023/24 season marked a sharp downturn, with production falling below 550,000 tonnes, the lowest level in two decades. This shortfall forced the postponement of about 370,000 tonnes in scheduled deliveries to international buyers, straining both export earnings and industry confidence. Looking ahead, the official target for 2024/25 is an ambitious recovery to between 650,000 and 700,000 tonnes, with expected exports of around 520,000 tonnes. In a normal production year, Ghana’s cocoa industry generates roughly $2 billion in foreign exchange and directly sustains the livelihoods of approximately 800,000 farm families, making it one of the most critical sectors in the national economy.

The recent production slump was the result of a combination of structural and environmental pressures. Swollen-shoot virus disease has devastated significant portions of the tree stock, erratic rainfall patterns have disrupted flowering and harvest cycles, and illegal mining activities, known locally as galamsey, have encroached on prime cocoa-growing land. Compounding these issues, a disparity in farm-gate prices between Ghana and neighboring Côte d’Ivoire encouraged smuggling, leading to lost volumes in official channels and a reduction in tax revenues. The government’s recovery strategy in 2025 hinges on accelerated replanting with disease-resistant varieties, targeted extension services, and upward adjustments in farm-gate prices to incentivize farmers to sell through legal, traceable channels.

Despite recent challenges, cocoa remains a cornerstone of Ghana’s fiscal and rural economic stability, not only providing livelihoods but also serving as a vital source of budget financing through the Ghana Cocoa Board (COCOBOD). The sector’s tax contributions fund essential public services and are integral to debt servicing in a strained macroeconomic environment. Stabilizing production will require parallel investments in traceability systems to meet the European Union’s deforestation-free regulation (EUDR) standards, ensuring continued access to the country’s largest export market. If Ghana can successfully combine disease control, farm rehabilitation, and market compliance, it stands to restore both its production levels and the fiscal flows that underpin national development priorities.

1. Côte d’Ivoire

Côte d’Ivoire remains the undisputed leader in global cocoa production, delivering an estimated 2.38 million tonnes in 2023 according to FAO data, accounting for over 40% of the world’s supply. However, the 2024/25 season has been marked by a significant drop in output to between 1.75 and 1.8 million tonnes, driven by adverse weather conditions and disease pressures. The industry is already preparing for tighter export allocations of roughly 1.3 million tonnes in 2025/26, as large-scale orchard regeneration programs take precedence over immediate volume. Despite these cyclical downturns, cocoa remains the backbone of Ivorian agriculture, underpinning both export earnings and the livelihoods of millions of rural households across the country’s cocoa belt.

The sector’s challenges are multifaceted. Aging tree stock and the spread of swollen-shoot disease have reduced productivity, while climate variability has disrupted flowering and harvest schedules. Additionally, high global prices in recent years have fueled smuggling to neighboring countries, where price differentials can be exploited, thereby eroding official sales volumes and tax revenues. The government’s current policy agenda targets accelerated replanting with disease-resistant varieties, expansion of farmer training, and stricter traceability measures to comply with the European Union’s deforestation-free regulation (EUDR). Meeting these compliance requirements is critical, as the EU remains Côte d’Ivoire’s largest export destination, and failure to adapt could jeopardize market access and premium pricing opportunities.

At the macroeconomic level, cocoa is a pillar of foreign exchange generation and a major driver of economic activity in the West African Economic and Monetary Union’s (WAEMU) largest economy. Even with recent production declines, cocoa’s economic footprint extends well beyond farming, supporting value chains in transport, warehousing, finance, and domestic processing. The government’s push to expand grinding capacity, already among the highest in Africa, is central to its strategy of retaining more value within national borders. By coupling sustained orchard renewal with greater investment in domestic value addition, Côte d’Ivoire can strengthen resilience against global market volatility, preserve its leadership position in the cocoa trade, and ensure that the sector continues to serve as a cornerstone of national development.

{kind=link}

Related News

How to Choose a Trustworthy Crypto Casino

Jan 22, 2026

Top Online Games Inspired by African Culture

Jan 22, 2026

Protecting Your Home’s Heart: The Importance of Reliable Water Lines

Jan 21, 2026