Table of Contents

Africa’s rising public debt has become one of the most persistent economic narratives of the past decade. From sovereign defaults and restructurings to IMF bailouts and ballooning interest payments, borrowing is often framed as evidence of fiscal indiscipline. Yet this interpretation oversimplifies a far more complex reality. African governments are not borrowing excessively because they are reckless, but because they are operating within structural constraints that make debt a central tool of state survival and development financing.

To understand why borrowing continues to rise across the continent, it is necessary to look beyond headline debt ratios and examine the deeper economic, fiscal, and global forces at play.

10. The Development Financing Gap: Borrowing to Build What Revenue Cannot

At the most basic level, African governments borrow because domestic revenues are insufficient to meet development needs.

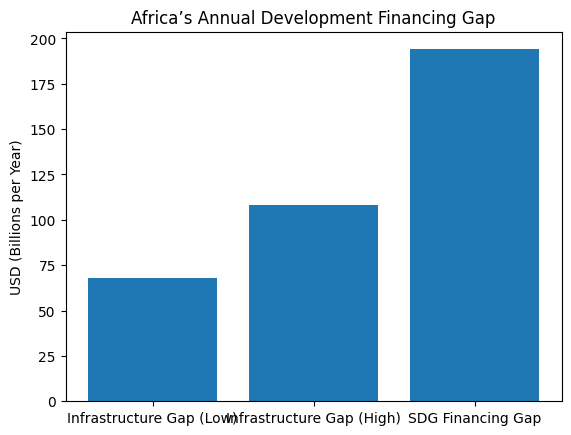

The continent faces one of the world’s largest infrastructure shortfalls. According to the African Development Bank (AfDB), Africa’s annual infrastructure financing gap ranges between $68 billion and $108 billion, covering roads, ports, railways, power generation, and water systems. These are not luxury projects, they are foundational investments required to unlock productivity and private-sector growth.

The challenge is timing. Infrastructure demands large upfront capital, while the economic returns materialize slowly over decades. With limited fiscal space, governments turn to debt to bridge that mismatch.

The problem extends beyond infrastructure. To meet the United Nations Sustainable Development Goals (SDGs) by 2030, Africa requires an estimated $194 billion in additional annual financing. Education, healthcare, sanitation, climate adaptation, and digital connectivity all require sustained spending that far exceeds current public revenues.

Borrowing, in this context, is not an aberration; it is the only available option.

Africa’s borrowing is largely driven by persistent development financing gaps, particularly in infrastructure and SDG-linked spending.

9. Weak Domestic Revenue Mobilization

Africa’s borrowing problem is inseparable from its chronic revenue constraints.

The average tax-to-GDP ratio across African economies stands at roughly 16 percent, the lowest of any region globally. In comparison, Latin America averages around 22 percent, while OECD economies exceed 34 percent.

Several factors explain this gap:

- Large informal economies that are difficult to tax

- Narrow tax bases dominated by consumption rather than income

- Weak tax administration and enforcement capacity

- Political resistance to broadening taxation

The result is a structural imbalance. Governments face growing populations, rising urbanization, and increasing service demands yet lack the revenue tools to fund them sustainably. Borrowing becomes the path of least resistance.

In countries like Kenya, Ghana, and Nigeria, public spending pressures have grown faster than tax reforms, locking governments into repeated debt issuance cycles.

8. Currency Risk and Dollar-Denominated Debt

A critical but often underestimated driver of Africa’s debt burden is currency mismatch.

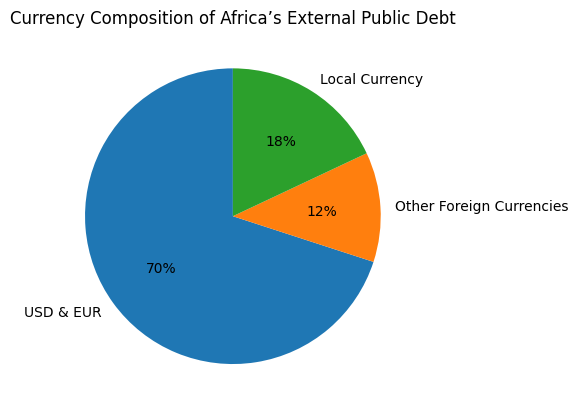

More than 70 percent of Africa’s public external debt is denominated in foreign currencies, primarily the US dollar. When local currencies depreciate, the real cost of servicing that debt rises sharply even if the original loan terms remain unchanged.

Nigeria offers a clear illustration. In 2024, the naira lost approximately 43 percent of its value, instantly inflating the local-currency cost of servicing dollar debt. Similar dynamics have played out in Egypt, Ghana, Zambia, and Malawi.

This currency exposure creates a vicious cycle:

- Currency depreciation raises debt-servicing costs

- Higher servicing costs widen fiscal deficits

- Larger deficits force governments to borrow more

What begins as an exchange-rate adjustment quickly becomes a debt spiral.

Heavy reliance on foreign-currency borrowing exposes African economies to exchange-rate shocks when local currencies depreciate.

7. Commodity Dependence and Volatile Export Earnings

Most African economies remain heavily dependent on raw commodity exports like oil, gas, minerals, and agricultural products for foreign exchange.

This dependence exposes public finances to global price swings beyond domestic control. When commodity prices fall, export revenues decline, foreign exchange reserves weaken, and governments struggle to meet external debt obligations.

The 2014 global commodity price crash sharply reduced revenues across oil-exporting countries such as Angola and Nigeria. More recently, global projections point to a 7 percent decline in commodity prices by 2026, threatening renewed fiscal stress.

Because debt is serviced in foreign currency, reduced export earnings directly undermine repayment capacity, forcing governments to borrow simply to stay current on existing obligations.

6. External Shocks and Crisis Borrowing

African borrowing has increasingly been shaped by crisis response rather than discretionary expansion. Over the last five years, governments have faced overlapping shocks , the COVID-19 pandemic, global supply-chain disruptions, and food and fuel price surges following the Russia–Ukraine war. Each shock forced emergency fiscal intervention.

IMF Fiscal Monitor data shows that sub-Saharan Africa’s average fiscal deficit widened sharply between 2020 and 2022, with governments borrowing to finance healthcare systems, vaccine procurement, food subsidies, and emergency income support. These were not growth-enhancing investments but stabilisation measures designed to prevent social and economic collapse.

Because these shocks are recurrent rather than exceptional, emergency borrowing has become embedded in fiscal planning, turning debt into a permanent shock-management instrument.

5. The Shift from Concessional to Commercial Credit

One of the most consequential shifts in Africa’s debt profile has been the move away from low-interest concessional loans toward commercial borrowing.

In 2010, private creditors held roughly 30 percent of Africa’s external public debt. By 2021, that share had risen to over 44 percent. Eurobonds, syndicated loans, and private placements now dominate new borrowing.

Unlike multilateral loans, commercial debt:

- Carries higher interest rates

- Has shorter maturities

- Offers little flexibility during crises

This shift dramatically increased refinancing risks, especially when global interest rates began rising after 2022.

4. Punitive Interest Rates and Credit Rating Constraints

African countries borrow at some of the highest sovereign interest rates in the world.

While G7 economies routinely issue debt at 2–3 percent, African sovereigns often face rates exceeding 10 percent, even during periods of global liquidity.

African leaders and the African Union have repeatedly criticized global credit rating agencies for overstating risk. Downgrades such as Fitch’s 2026 downgrade of Afreximbank can sharply raise borrowing costs overnight, regardless of underlying economic fundamentals.

High interest costs mean that a significant share of new borrowing goes not toward development, but toward servicing old debt.

3. The Domestic Debt Boom and Crowding-Out Effect

To reduce foreign exchange risk, many African governments have turned inward, dramatically expanding domestic debt markets.

Since 2010, domestic public debt has nearly tripled to about $500 billion. While this reduces currency exposure, it comes at a cost.

Domestic bonds often carry nominal yields of 10–13 percent, making them expensive. Worse, they absorb capital that might otherwise flow to private businesses, stifling investment and job creation.

Banks increasingly prefer lending to governments rather than enterprises, deepening structural economic weakness.

2. Governance Failures and Inefficient Public Spending

Debt accumulation is intensified by corruption, mismanagement, and weak project execution.

Numerous studies show a strong correlation between high corruption levels and rising public debt. When borrowed funds fail to translate into productive assets, governments are left servicing liabilities without corresponding growth benefits.

Delayed projects, inflated contracts, and poorly targeted subsidies weaken the growth-debt relationship, forcing governments to borrow again to compensate for lost momentum.

1. The Refinancing Treadmill: Borrowing to Pay the Past

At the core of Africa’s debt problem lies a harsh reality: many countries are borrowing not to invest, but to survive.

Short-term maturities and high interest rates have trapped governments in a refinancing loop. New loans are increasingly used to pay off maturing obligations rather than fund new projects.

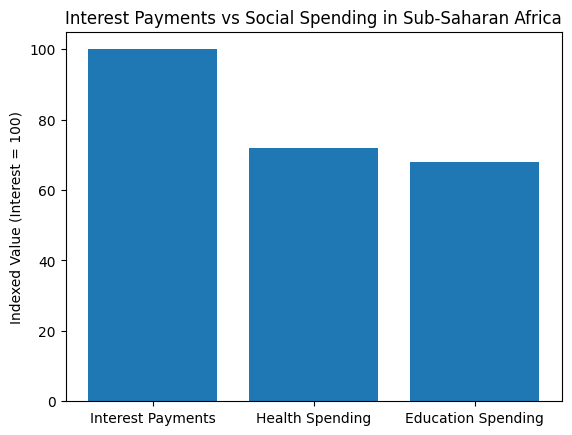

In over half of Sub-Saharan Africa, governments now spend more servicing debt than on health or education, constraining human capital investment.

By 2023, more than half of Sub-Saharan Africa’s population lived in countries spending more on interest payments than on health or education. This represents not just a fiscal crisis, but a developmental one.

Conclusion: A Systemic Problem, Not a Continental Failure

Africa’s debt crisis is often framed as a story of poor decisions. In reality, it is the outcome of structural constraints, external vulnerabilities, and a global financial system that prices African risk aggressively.

Advanced economies built their infrastructure and welfare states through decades of affordable borrowing. Africa is attempting the same but under far harsher financial conditions, at higher interest rates, and with less margin for error.

Until the global financing system changes, Africa’s debt problem is not an exception; it is the default outcome of how development is currently financed.

{kind=link}