Table of Contents

U.S. foreign direct investment into Africa has entered a structurally different phase. Unlike earlier cycles dominated by oil and legacy extractives, recent data from the U.S. Bureau of Economic Analysis (BEA), UNCTAD, FDI Intelligence, and the U.S. International Development Finance Corporation (DFC) show that American capital is increasingly strategic, selective, and long-term.

Between 2024 and 2025, U.S. outward FDI stock in Africa expanded steadily, supported by energy-transition investments, critical-mineral security concerns, digital infrastructure expansion, and industrial reshoring strategies linked to global supply-chain realignment. By 2026, this shift has crystallized into a clear hierarchy of African destinations receiving the largest volumes of U.S.-sourced equity investment, rather than total global FDI.

This ranking prioritizes recent and projected FDI inflows (2024-2026) involving U.S. investors, drawing on UNCTAD World Investment Reports (2024-2025), U.S. Bureau of Economic Analysis (BEA), Reuters deal tracking, Development Finance Corporation (DFC) disclosures, and African central bank data. Stock data is used contextually, not as the ranking driver, to show depth and sustainability of U.S. capital presence.

Foreign direct investment inflows vary across African regional groupings, reflecting diverse economic strengths and investor priorities. Source: UNCTAD World Investment Report 2025.

10.Senegal

Senegal’s FDI story heading into 2026 reflects a progressive diversification of foreign investment, including increased interest from U.S. corporations and global capital seeking to tap into West Africa’s emerging market growth. According to the UNCTAD World Investment Report series, Senegal’s inward FDI rose from around US$1.06 billion in 2019 to about US$2.64 billion in 2023, highlighting a sustained expansion of capital flows driven by infrastructure, energy, and services projects.

Senegal’s attractiveness to U.S. and other foreign investors is rooted in robust political stability, market reforms, and strategic location, paired with targeted infrastructure investments that enhance regional connectivity. Projects such as the Port of Ndayane, being developed by international terminal operators, and advanced oil and gas developments in the Sangomar basin illustrate how Senegal’s project pipeline draws investment that often involves multinational participation, including Western energy firms and capital partners.

In addition to hydrocarbons, FDI into Senegal increasingly includes renewable energy, agribusiness, and services. Improved business facilitation under the country’s investment code and a one‑stop shop for investor services have shortened licensing timelines and enhanced predictability for inbound capital, while regional trade integration through WAEMU expands market access beyond Senegal’s borders. Although U.S. business interest is sometimes outpaced by European engagement due to historical ties, American firms and funds are participating in financing and technology partnerships, particularly in energy, infrastructure, and logistics sectors as part of broader financing syndicates and joint ventures with local partners.

Senegal’s economic growth prospects, projected at rates above regional averages due in part to expanded natural resource production and infrastructure development, further bolster the investment case for long‑term U.S. participation. As Senegal continues to build out its project ecosystem and institutional capacity, its standing as a competitive FDI destination including for U.S. capital is expected to solidify into 2026 and beyond.

9.Mauritius

Mauritius’s position in Africa’s FDI landscape is shaped by its status as a financial and services hub, which attracts diverse capital flows, including those linked to U.S. investment, even if its total annual FDI figures are modest compared with continental leaders. According to UNCTAD stat data, Mauritius recorded FDI inflows of approximately US$681.3 million in 2024, up from earlier lower levels in mid‑decade, underscoring the island’s role as a conduit and investment destination in the Indian Ocean and Southern Africa region.

Mauritius’s appeal to U.S. investors and global capital more broadly rests on its politically stable, open economy, and well‑developed legal framework that supports cross‑border investment and financial services. The country’s economy is dominated by services such as financial intermediation, tourism, and information technology, which in total account for over 70 percent of GDP and provide structural depth that helps attract and recycle foreign capital.

The island’s role as a regional investment gateway has been amplified by its network of double taxation treaties and investment protection agreements, which make it a preferred jurisdiction for U.S. and European investors targeting broader African opportunities. U.S. private equity and asset management firms use Mauritius‑based vehicles to structure investments into East and Southern Africa, particularly in sectors such as renewable energy, technology platforms, and regional logistics. Although direct U.S. FDI numbers specifically into Mauritius are not always large in headline terms, the country functions as a financial hub that supports significant indirect and structured investment flows within Africa.

Going into 2026, Mauritius’s strategy focuses on deepening its services ecosystem, enhancing fintech and digital hubs, and leveraging its geographic and policy advantages to remain a compelling base for U.S. investors seeking Africa exposure through structured investment platforms.

8.Ghana

Ghana’s foreign direct investment profile heading into 2026 reflects a notable rebound in investor confidence, underpinned by macroeconomic reforms, debt restructuring, and renewed project activity in industry and trade. According to data from the Ghana Investment Promotion Centre (GIPC), total registered FDI in the first half of 2025 surged to approximately US$862.9 million, a dramatic 382 percent increase compared with the same period in 2024, underscoring a strong capital inflow trend as the country stabilizes after macroeconomic adjustments.

The composition of Ghana’s FDI inflows illustrates a diversifying investment landscape. While manufacturing accounted for the highest number of new registered projects (32 out of 76 between January and June 2025), general trading drew the largest share of investment value (US$622.92 million), reflecting commercial and distribution expansion in the Ghanaian economy. U.S. firms have been part of this ecosystem, participating in sectors such as financial services and technology through strategic equity stakes and partnerships, although China and India were larger sources of the new project count in this period.

Investor sentiment toward Ghana has improved due to structural policy reforms supported by the International Monetary Fund and domestic fiscal consolidation measures that have restored some macro stability after earlier debt distress. These reforms combined with improvements in regulatory transparency and investment facilitation have encouraged both African and Western investors to deepen engagement in key sectors such as manufacturing, services, agribusiness, and digital technologies. As Ghana continues to advance economic diversification and strengthen institutions, its FDI base, including U.S. investment, is poised to grow sustainably, making it an increasingly attractive destination for long‑term capital flows into West Africa.

7.Kenya

Kenya has established itself as a resilient and increasingly diversified destination for U.S.-linked foreign direct investment, combining regional connectivity, a growing tech ecosystem, and long-standing trade partnerships. According to UNCTAD and the Kenya National Bureau of Statistics (KNBS), Kenya attracted approximately US$2.2–2.5 billion in FDI in 2024, with U.S. investors concentrating on technology, renewable energy, infrastructure, and agribusiness. The country’s strategic position as East Africa’s commercial and logistics hub, anchored by Nairobi and Mombasa, continues to make it a preferred entry point for U.S. capital seeking regional reach.

U.S. investment in Kenya spans several decades, but it accelerated in the mid-2000s following the African Growth and Opportunity Act (AGOA), which provided preferential access to U.S. markets. American firms have been particularly active in information technology, fintech, renewable energy, and export-oriented agriculture, reflecting both opportunity and alignment with U.S. strategic priorities in innovation, green energy, and food security. Nairobi’s tech ecosystem, famously dubbed “Silicon Savannah,” has attracted venture capital and private equity from U.S. firms like Sequoia, Google Ventures, and Accel, particularly targeting fintech, e-commerce, and digital infrastructure.

Energy and infrastructure remain key pillars of U.S. engagement. American development finance institutions and private investors have backed solar, wind, and hydroelectric projects, complementing the government’s Kenya Vision 2030 industrialization plan. The Lake Turkana Wind Power Project, partially financed through U.S. DFC and private equity, and the Mombasa port expansion are flagship projects that highlight both long-term equity commitments and strategic interest in regional logistics.

Kenya’s appeal is underpinned by relative political stability, an investment-friendly regulatory environment, and integration into regional trade blocs such as the East African Community (EAC). However, challenges such as regulatory delays, currency volatility, and infrastructure gaps persist, shaping the scope and structure of U.S. investment. Analysts note that U.S. inflows tend to be strategic and long-term, with a focus on sectors offering both financial returns and regional influence.

Looking forward into 2026, Kenya is poised to continue attracting U.S.-linked FDI, particularly in technology-led services, renewable energy expansion, and logistics infrastructure. Its combination of market access, skilled labor, and regulatory clarity ensures that American investors view Kenya not only as a destination for capital deployment but also as a gateway for scaling operations across East Africa.

6.Democratic Republic of Congo (DRC)

The Democratic Republic of Congo (DRC) has emerged as a strategic, if high-risk, destination for U.S.-linked foreign direct investment heading into 2026, primarily driven by the global demand for critical minerals and energy resources. According to UNCTAD’s World Investment Report 2025 and Dab finance Africa FDI Monitor, the DRC attracted approximately US$3.1 billion in FDI in 2024, with U.S. investors increasingly participating in mining, energy, and related infrastructure projects. While a substantial portion of inflows continues to be commodity-centric, the U.S. has played a growing role in structuring financing for strategic assets linked to copper, cobalt, lithium, and gold essential inputs for electric vehicles (EVs) and renewable energy technologies.

American investment in the DRC has intensified over the past decade, with a notable uptick after 2015, as global EV demand and energy transition imperatives heightened interest in African supply chains. Major U.S.-linked firms and private equity funds have participated in equity stakes and joint ventures with global miners such as Ivanhoe Mines and Zijin Mining, focusing on expanding production capacity at projects like Kamoa-Kakula and developing downstream processing facilities for battery-grade cobalt and copper. Development finance from the U.S. International Development Finance Corporation (DFC) and technical support from USAID have been leveraged to de-risk investments, particularly in energy infrastructure and logistics upgrades necessary for large-scale mining operations.

Despite the strong resource base, investment in the DRC remains highly concentrated and risk-sensitive. Political instability, regulatory unpredictability, and infrastructure bottlenecks limit broader U.S. participation outside major mega-projects. Data from the Central Bank of Congo (BCC) and the World Bank’s 2025 country update underscore that while flagship mining ventures drive the bulk of inflows, smaller investors face bureaucratic hurdles and security risks. However, recent reforms under the Mining Code and investment promotion frameworks, including fiscal incentives and guaranteed partnership rights, have improved transparency and partially stabilized investor sentiment.

Looking into 2026, the DRC is expected to maintain its position as a leading U.S.-linked FDI destination in Central Africa. Ongoing initiatives in renewable energy, local value addition, and transport infrastructure aim to complement extractive investments, while global investors continue to prioritize the country for its indispensable role in securing minerals critical for the clean energy transition.

5.Morocco

Morocco has quietly become one of Africa’s most sophisticated and reliable destinations for U.S. foreign direct investment, combining political stability, export-oriented industrial policy, and deep integration with Western supply chains. According to UNCTAD and Moroccan Foreign Exchange Office data, Morocco attracted approximately US$3.6–3.9 billion in FDI in 2024, with U.S. firms accounting for a growing share of manufacturing, aerospace, automotive, and renewable energy investment. Unlike commodity-driven FDI hubs, Morocco’s appeal lies in its ability to consistently convert policy clarity into long-term industrial capital.

U.S. investment in Morocco has roots stretching back over two decades, significantly reinforced by the U.S.–Morocco Free Trade Agreement (FTA) that came into force in 2006. This agreement eliminated most tariffs, strengthened investor protections, and gave American firms preferential access to a stable North African manufacturing base with direct proximity to Europe. Since then, U.S. multinationals have expanded across aerospace components, automotive wiring systems, industrial machinery, and agribusiness processing, embedding Morocco into transatlantic and Euro-Mediterranean value chains.

In recent years, Morocco’s industrial zones and export platforms have been the primary magnets for U.S. capital. The Tanger-Med industrial and logistics complex, now one of Africa’s largest ports, has attracted U.S.-linked manufacturers and logistics operators seeking efficient access to European markets. According to Reuters investment tracking and Moroccan Investment and Export Development Agency data, American firms have increasingly favored Morocco as a “near-shoring” destination amid global supply-chain reconfiguration.

Energy transition has emerged as a second major pillar of U.S. investment. Morocco’s aggressive push into solar, wind, and green hydrogen has aligned closely with U.S. strategic priorities around climate finance and clean-energy supply chains. American development finance institutions and private equity funds have participated in renewable energy projects and feasibility studies linked to hydrogen exports to Europe. Data from the International Energy Agency and the U.S. Department of State confirm Morocco’s role as a priority partner in clean-energy cooperation across North Africa .

Morocco’s competitive edge for U.S. investors lies in predictability. Strong institutions, investment-friendly regulation, currency stability, and efficient export logistics reduce execution risk compared with many emerging markets. While Morocco’s domestic consumer market is smaller than Nigeria’s or Egypt’s, U.S. investors view the country less as a demand play and more as a production and export hub. As global firms rebalance exposure away from Asia-centric supply chains, Morocco’s relevance in U.S. FDI strategy continues to rise.

Heading into 2026, Morocco is expected to retain its position among Africa’s top U.S. FDI destinations, supported by manufacturing expansion, renewable energy scale-up, and its unique status as a bridge between Africa, Europe, and the United States. Its experience underscores a broader trend in U.S. investment behavior: capital increasingly follows governance quality, trade access, and supply-chain resilience rather than market size alone.

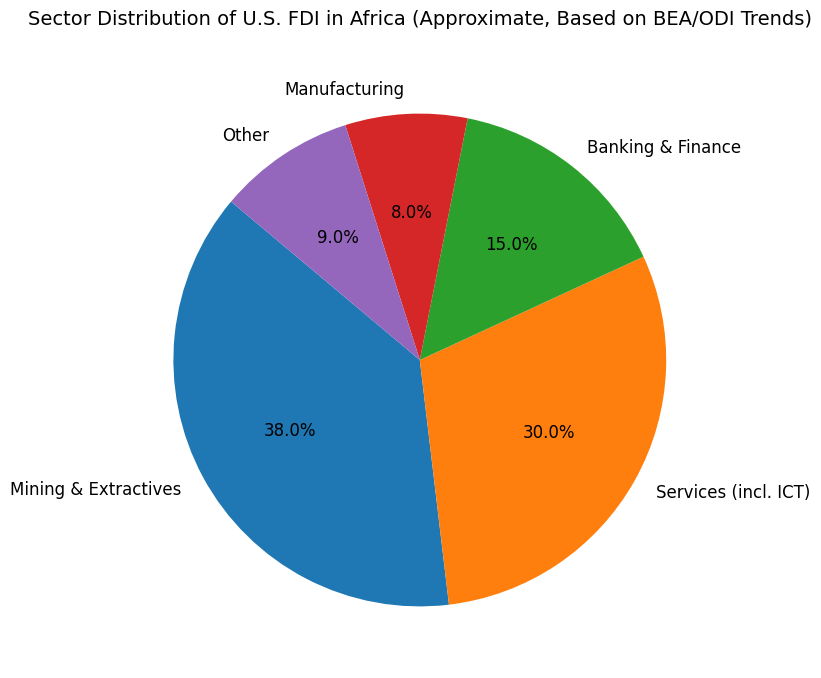

Sector Distribution of U.S. FDI in Africa (Approximate, Based on BEA and ODI Reports, 2024–2025). Mining & Extractives dominate with 38%, followed by Services including ICT at 30%, Banking & Finance at 15%, Manufacturing at 8%, and Other sectors at 9%

4.Ethiopia

Ethiopia has steadily consolidated its position as one of Africa’s most strategically significant destinations for the U.S.-linked foreign direct investment heading into 2026, driven less by short-term capital surges and more by long-horizon industrial positioning. According to UNCTAD’s World Investment Report 2025, Ethiopia attracted approximately US$3.5–4.0 billion in inward FDI in 2024, placing it among the continent’s top five recipients. While U.S. capital does not dominate Ethiopia’s inflows numerically in the same way it does in Egypt or South Africa, American investment plays a disproportionately influential role in shaping priority sectors, particularly manufacturing, logistics, agribusiness, and energy.

U.S. engagement in Ethiopia accelerated meaningfully after 2018, following the country’s political opening and the launch of the Homegrown Economic Reform Agenda (HERA), which signaled a shift toward private-sector-led growth. American firms and development financiers began scaling exposure through export-oriented manufacturing, industrial parks, and supply-chain infrastructure designed to serve European and Middle Eastern markets. Companies operating in textiles, apparel, food processing, and light manufacturing have benefited from Ethiopia’s large labor pool, preferential trade access under the African Growth and Opportunity Act (AGOA) prior to suspension, and improving logistics connectivity through the Addis–Djibouti corridor.

A central pillar of U.S. involvement has been development-backed equity and project finance. The U.S. International Development Finance Corporation (DFC) has supported investments in renewable energy, industrial infrastructure, and SME finance, positioning Ethiopia as a long-term manufacturing and export platform rather than a purely consumer-driven market. According to DFC disclosures and World Bank project data, U.S.-linked financing has targeted power generation, off-grid solar, logistics platforms, and financial inclusion initiatives aimed at de-risking private capital entry .

Ethiopia’s appeal to U.S. investors is fundamentally structural. With a population exceeding 120 million, rapid urbanization, and one of Africa’s most ambitious industrialization agendas, the country offers a scale that few peers can match. However, U.S. investment has remained selective, shaped by macroeconomic constraints such as FX shortages, inflation, and debt pressures. Reforms underway in 2024–2025, including gradual exchange-rate liberalization, telecom sector opening, and partial privatization of state-linked enterprises, are closely watched by U.S. corporates and private equity funds evaluating deeper market entry.

Looking into 2026, Ethiopia’s role in U.S. FDI flows is expected to remain anchored in manufacturing relocation, energy transition infrastructure, and logistics, rather than headline megadeals. Analysts note that Ethiopia’s success in converting reform momentum into policy consistency will be decisive. If macro stabilization continues, Ethiopia is positioned to strengthen its standing as one of Washington’s most strategically important long-term investment partners in East Africa.

3. Nigeria

Nigeria retains its position as one of Africa’s most strategically important destinations for U.S. foreign direct investment flows, even as headline inflows fluctuate. According to Nigeria’s National Bureau of Statistics and UNCTAD estimates, Nigeria attracted between US$1.6 and US$2.0 billion in FDI in 2024, with U.S. capital concentrated in energy, financial services, and technology-enabled services rather than large greenfield manufacturing.

U.S. investment in Nigeria is primarily strategic and sector-specific, reflecting both opportunity and risk. In energy, American oil majors and service firms continue to maintain stakes in offshore production and gas infrastructure, even as some divest onshore assets. In parallel, U.S. venture capital and private equity have remained active in Nigeria’s fintech ecosystem, backing firms operating in payments, lending, and digital infrastructure serving Africa’s largest population. These investments are typically equity-heavy and long-term, favoring scalability over short-term returns.

Recent macroeconomic reforms, including FX liberalization and fuel subsidy removal, have reshaped Nigeria’s investment narrative. While these moves initially triggered volatility, they are increasingly viewed by U.S. investors as necessary corrections that improve long-term capital repatriation and pricing transparency. However, security challenges, regulatory unpredictability, and infrastructure gaps continue to constrain broader FDI diversification. Going into 2026, Nigeria’s ability to convert reforms into sustained inflows will determine whether it strengthens or merely maintains its standing among Africa’s top U.S. FDI recipients.

2. South Africa

South Africa remains one of Africa’s most consistent and structurally attractive destinations for U.S. foreign direct investment, combining steady inflows with the continent’s deepest pool of reinvested earnings. According to UNCTAD and South African Reserve Bank (SARB) data, South Africa recorded US$2.4–2.5 billion in FDI inflows in 2024, with momentum extending into 2025 through equity reinvestments, mergers and acquisitions, and renewable energy financing.

U.S. investment in South Africa is distinguished by sectoral breadth rather than megaproject dominance. American firms are deeply embedded across mining, financial services, automotive manufacturing, consumer goods, and technology. Companies such as Anglo American (U.S.-listed), Ford, Microsoft, Amazon Web Services, and Visa-linked fintech investors continue to expand operations, often reinvesting profits rather than entering through greenfield projects. The Johannesburg Stock Exchange (JSE) functions as a regional capital gateway, enabling U.S. investors to scale exposure across Southern Africa.

Energy transition financing has become a critical driver of recent inflows. Under the Just Energy Transition framework, U.S. development finance institutions and private equity funds have supported solar, wind, and grid infrastructure projects, partially offsetting concerns over Eskom’s power constraints. While persistent electricity shortages, logistics bottlenecks, and regulatory uncertainty dampen short-term sentiment, South Africa’s institutional depth, legal predictability, and corporate governance standards continue to anchor U.S. investment decisions. Heading into 2026, South Africa remains a low-replacement-risk destination for U.S. capital despite rising competition from North African and East African markets.

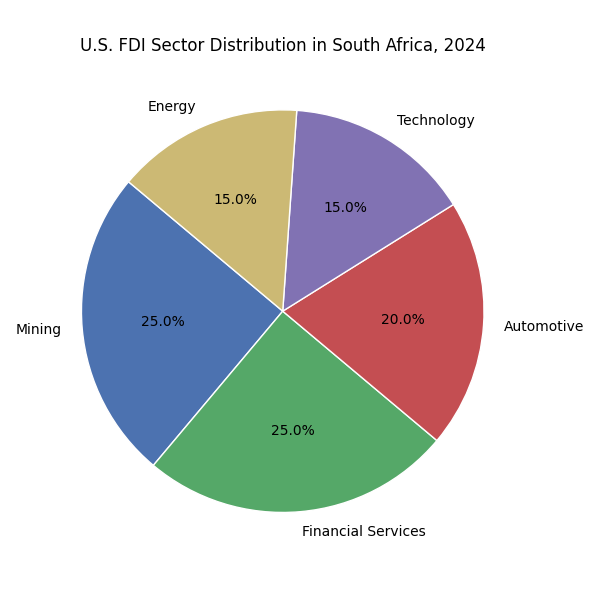

Sectoral Breakdown of U.S. Foreign Direct Investment in South Africa, 2024. Mining and Financial Services lead, followed by Automotive, Technology, and Energy

1. Egypt

Egypt stands as Africa’s largest recipient of U.S.-linked foreign direct investment flows heading into 2026, driven by an exceptional concentration of large-scale equity-backed megaprojects, energy investments, and strategic infrastructure deals. UNCTAD’s World Investment Report 2025 places Egypt’s total inward FDI at approximately US$46 -- 46.6 billion in 2024, the highest on the continent, with U.S., Gulf, and European capital jointly underpinning the surge. While not all inflows are exclusively American, U.S. institutional investors, private equity funds, and multinational firms played a central role in structuring and financing several of the year’s largest projects.

A defining feature of Egypt’s recent inflows is the scale of project-based equity, particularly in real estate, tourism, logistics, and energy along the Mediterranean and Red Sea corridors. The Ras El-Hekma coastal development and associated infrastructure upgrades attracted global capital pools, including U.S.-aligned investment vehicles seeking long-term exposure to tourism, urban development, and logistics hubs connecting Africa, the Middle East, and Europe. U.S. energy companies and funds also remain active in Egypt’s upstream gas sector and renewable energy pipeline, supported by regulatory reforms and long-term production-sharing agreements.

Beyond megaprojects, Egypt’s appeal to U.S. investors lies in market depth and policy positioning. With over 110 million consumers, improving FX liquidity after IMF-supported reforms, and a state-led push to monetize state assets, Egypt offers scale unmatched elsewhere in Africa. However, analysts caution that Egypt’s headline inflows are highly concentrated, making year-on-year figures volatile. While 2026 is unlikely to replicate 2024’s extraordinary totals, Egypt’s baseline for U.S.-linked FDI has structurally shifted upward, cementing its position at the top of Africa’s FDI hierarchy.

Conclusion

The landscape of U.S. foreign direct investment in Africa in 2026 reflects both continuity and strategic recalibration. Egypt, South Africa, and Nigeria remain the continent’s most prominent recipients, demonstrating the enduring appeal of large-scale megaprojects, diversified sectoral exposure, and institutional depth. Meanwhile, countries such as Ethiopia, Morocco, Kenya, Ghana, Mauritius, Senegal, Uganda, Mozambique, and the DRC illustrate the breadth of U.S. engagement across industrialization, energy transition, infrastructure, and technology-led development. U.S. investors have increasingly prioritized sectors that promise long-term scalability and regional influence, including energy, financial services, manufacturing, agribusiness, and digital infrastructure, often leveraging development finance frameworks, public-private partnerships, and equity reinvestments.

The investment patterns also highlight a nuanced risk-reward calculus. While countries with macroeconomic stability, robust governance, and market depth attract predictable flows, resource-rich or reforming economies continue to draw targeted project-based investments, often tied to commodity cycles or infrastructure modernization. Strategic U.S. capital deployment has not only injected equity but also encouraged local capacity building, technology transfer, and regional integration, reinforcing the multiplier effect of FDI beyond immediate financial inflows.

Looking forward, Africa’s U.S.-linked FDI trajectory will likely remain sectoral concentrated yet geographically diversified. Governments that combine transparent regulations, investor-friendly incentives, and targeted sectoral development stand to secure sustainable inflows, even amid global economic volatility. For U.S. investors, the continent represents a mosaic of opportunities-from established economic hubs to emerging markets-each offering distinct entry points, operational considerations, and long-term growth potential. In sum, the 2026 FDI landscape underscores Africa’s rising significance in global capital allocation, with the United States positioned as a key partner in shaping the continent’s industrial, technological, and energy futures.

%20in%202026){kind=link}