Table of Contents

In Summary:

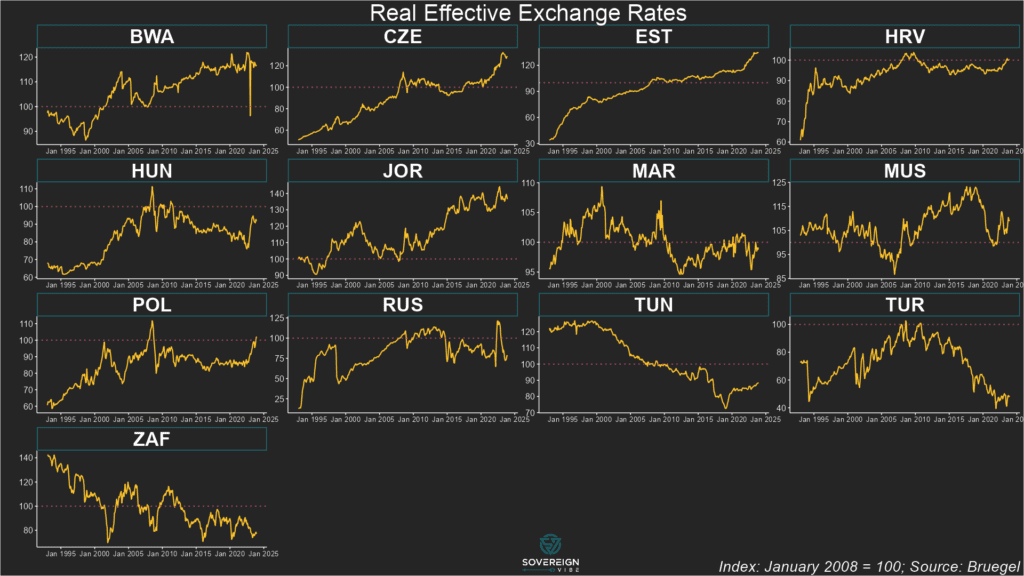

- The Real Effective Exchange Rate (REER), which adjusts for inflation and trade weights, is a more meaningful indicator of currency stability than headline nominal exchange rates.

- Top-ranked currencies achieve stability via different mechanisms, including hard pegs (CFA Franc, Cape Verde Escudo), managed floats (Moroccan Dirham), and disciplined independent policy (Rwandan Franc).

- Regardless of the exchange rate regime, low and stable inflation, prudent fiscal management, and strong institutional frameworks are the universal prerequisites for REER stability.

- The highest stability often comes at the cost of surrendering monetary policy autonomy, requiring even greater fiscal discipline to maintain economic equilibrium.

Deep Dive!!

17 December 2025 – In the volatile landscape of global finance, currency stability is a critical indicator of a nation's economic health and policy credibility. While nominal exchange rates against the US Dollar or Euro grab headlines, economists and policymakers pay closer attention to the Real Effective Exchange Rate (REER). The REER measures a currency's value against a weighted basket of trading partners' currencies, adjusted for inflation differentials. A stable REER over time suggests a currency is neither becoming too overvalued (hurting exports) nor too undervalued (sparking inflation), reflecting sound macroeconomic fundamentals and effective monetary policy.

This analysis, drawing on data and reports from the International Monetary Fund (IMF), the World Bank, and regional bodies like the African Development Bank (AfDB), identifies the African currencies with the most stable REER over the recent five-year period (2019-2024). Stability is measured by low volatility in REER indices, sustained within a manageable band, indicating resilience to external shocks like commodity price swings and global monetary tightening. The ranking considers economies with diverse structures, from resource-rich nations to service-oriented hubs, highlighting those that have best managed the complex balance of trade, inflation, and capital flows.

10. Ghanaian Cedi (GHS)

The inclusion of the Ghanaian Cedi highlights a nuanced reality: recent stability following a profound adjustment. After a period of significant depreciation driven by fiscal imbalances and loss of market access, the Cedi's REER found a new, more sustainable equilibrium following the 2023 domestic debt exchange and an IMF Extended Credit Facility program. While its nominal value remains under pressure, the inflation-adjusted REER has shown markedly reduced volatility since mid-2023, indicating the sharp correction may have overshot fundamentals. The Bank of Ghana's tighter monetary policy and improved foreign exchange liquidity have been crucial in anchoring expectations and stabilizing the real rate, though long-term stability remains contingent on sustained fiscal discipline.

Ghana's journey underscores that REER stability can emerge from a painful recalibration. The currency's real value is now more aligned with its economic fundamentals, aided by structured multilateral support. Stability going forward is fragile and highly dependent on the successful continuation of its IMF program, external debt restructuring, and a return to sustainable fiscal policy. The Cedi ranks tenth as a case study in stabilization from a low base, with its position reflecting recent improvement rather than long-standing resilience.

9. Ugandan Shilling (UGX)

The Ugandan Shilling has demonstrated notable resilience and low volatility in its REER, supported by a consistent and conservative monetary policy framework from the Bank of Uganda (BoU). Uganda maintains a flexible exchange rate regime, but the BoU's focus on controlling inflation, keeping it within single digits for extended periods, has been the primary anchor for the Shilling's real value. The economy's relative diversification, with robust contributions from agriculture, services, and now emerging oil sector prospects, provides a natural hedge against external shocks, reducing wild swings in the trade balance that could destabilize the REER.

Uganda's REER stability benefits from limited reliance on portfolio flows ("hot money"), which can cause sudden stops and reversals. However, the commencement of oil production and related imports pose a new structural shift that the BoU will need to manage carefully to avoid Dutch Disease effects, where resource inflows cause real exchange rate appreciation that harms other exports. Maintaining the current policy mix will be key to preserving the Shilling's stable real value as the economic structure evolves.

8. Tanzanian Shilling (TZS)

The Tanzanian Shilling is often cited as one of East Africa's most stable currencies, a characteristic reflected in its steady REER. This stability stems from sustained macroeconomic stability, moderate inflation, and a current account deficit that has been manageable and largely financed by foreign direct investment (FDI) rather than volatile debt flows. The Bank of Tanzania's (BoT) pragmatic approach, involving strategic interventions to smooth excessive volatility without defending a fixed level, has proven effective. Furthermore, Tanzania's economic growth, driven by agriculture, tourism, and infrastructure projects, has been consistent, avoiding boom-bust cycles that destabilize currencies.

Tanzania's REER stability is a product of cautious economic management. However, the country's increasing public investment in mega-projects requires careful monitoring of external borrowing to prevent future debt-service pressures on the Shilling. The BoT's challenge will be to maintain its disciplined intervention policy while navigating global financial conditions. Its track record suggests a capacity to manage these pressures, supporting a forecast of continued low REER volatility.

7. Rwandan Franc (RWF)

The Rwandan Franc's REER stability is a testament to the government's disciplined and reform-oriented macroeconomic management. Rwanda has maintained low and stable inflation, averaging around 2-5% in recent years, which is the critical domestic adjustment factor in the REER calculation. The National Bank of Rwanda (BNR) operates a flexible exchange rate but is proactive in building robust foreign exchange reserves as a buffer. While Rwanda runs a persistent trade deficit, it is consistently financed by stable inflows of aid, FDI, and remittances, creating predictable balance of payments support that prevents abrupt REER adjustments.

Rwanda's small, landlocked economy is inherently vulnerable to terms-of-trade shocks. Its REER stability is therefore a hard-won achievement of policy credibility. The main risk to this stability is the potential for faster-than-expected tightening of global financial conditions, which could affect the availability of external financing. Nonetheless, the BNR's strong institutional framework and commitment to a market-determined rate within a stable macroeconomic context position the Franc for continued real stability.

6. Botswana Pula (BWP)

The Botswana Pula operates under a unique and stable managed float, pegged to a basket of currencies heavily weighted toward the South African Rand (ZAR) and the IMF's Special Drawing Rights (SDR). This explicit basket peg provides a transparent and effective nominal anchor, which directly translates into REER stability. As a major diamond exporter, Botswana accumulates substantial foreign exchange reserves during commodity booms, which it deftly uses to smooth Pula fluctuations during downturns. This prudent sovereign wealth management, embodied in the Pula Fund, insulates the domestic economy and the currency's real value from the full brunt of diamond price volatility.

Botswana's REER stability is institutionalized through its currency basket and fiscal rule framework. Its primary vulnerability is its close linkage to the South African Rand; economic or political shocks in South Africa transmit directly to the Pula. However, Botswana's superior fiscal position and massive reserves provide an unmatched buffer, allowing it to maintain stability where other commodity exporters might fail. This makes the Pula a pillar of real exchange rate consistency in Southern Africa.

5. Namibian Dollar (NAD)

The Namibian Dollar's stability is fundamentally anchored by its longstanding and legally enforced currency peg to the South African Rand at a 1:1 ratio. As part of the Common Monetary Area (CMA), Namibia cedes independent monetary policy to the South African Reserve Bank (SARB). This arrangement eliminates nominal exchange rate volatility against its largest trading partner, which constitutes a massive share of its trade. Consequently, Namibia's REER stability is primarily a function of its imported price stability from South Africa and its own disciplined fiscal policy, which keeps domestic inflation closely aligned with South Africa's.

The NAD's peg is a double-edged sword. It provides exceptional stability and facilitates trade but removes crucial policy tools. Namibia cannot devalue to regain competitiveness, making domestic productivity and fiscal restraint the only adjustment mechanisms. Therefore, its REER stability is contingent on maintaining fiscal prudence to avoid building imbalances that the peg itself could exacerbate. As long as the CMA holds and South Africa maintains relative macroeconomic stability, the NAD will remain among the continent's most stable real currencies.

4. Seychellois Rupee (SCR)

The Seychellois Rupee presents a remarkable case of a small island economy achieving REER stability through exemplary policy reform. Following a dramatic economic crisis and currency devaluation in 2008, Seychelles implemented a stringent IMF program, adopted a floating exchange rate, and established a highly credible central bank. The Central Bank of Seychelles' unwavering commitment to a market-determined rate and inflation targeting has paid dividends. Tourism, a stable source of foreign exchange, funds the import-dependent economy, and the flexible rate acts as a natural shock absorber, preventing major REER misalignments.

Seychelles demonstrates that for small, open economies, a credible float can be the surest path to REER stability. Its success is built on strong institutions, substantial reserve buffers, and a dominant export sector (tourism) with reliable demand. Vulnerabilities include exposure to global travel shocks (as seen during COVID-19) and climate change impacts. However, the SCR's proven resilience and the credibility of its monetary framework suggest a continued path of low real exchange rate volatility.

3. Moroccan Dirham (MAD)

The Moroccan Dirham benefits from a carefully managed float within a steadily widening band, a system overseen by Bank Al-Maghrib (BAM). This regime allows for gradual, predictable adjustment while shielding the economy from speculative attacks. Morocco's diverse economy, spanning phosphates, agriculture, automotive manufacturing, and tourism, provides natural diversification against sector-specific shocks. Crucially, the country has maintained low budget deficits, moderate inflation, and a current account deficit that is comfortably financed by remittances and FDI, all of which underpin confidence in the Dirham's real value.

Morocco's gradual move toward greater exchange rate flexibility is a textbook example of a well-sequenced reform. By slowly widening the trading band, BAM is allowing the market a greater role without surrendering control, a process that enhances the Dirham's resilience. The country's strategic trade agreements with the EU and the US also provide a stable external environment. Barring a major regional or commodity shock, the Dirham's REER is poised to remain a benchmark of stability in North Africa.

2. Cape Verdean Escudo (CVE)

The Cape Verdean Escudo holds a uniquely stable position due to its long-standing and unshakable peg to the Euro. As a former Portuguese colony with an economy deeply integrated with the Eurozone (reliant on tourism, remittances, and aid), this peg provides an unparalleled nominal anchor. The peg is backed by a currency board-like arrangement with Portugal, ensuring full convertibility and absolute commitment. This structure imports the monetary policy credibility of the European Central Bank, resulting in inflation rates and a REER that move in lockstep with those of its Eurozone partners.

The CVE's stability is absolute but comes with the classic constraints of a hard peg. Cape Verde has no independent monetary policy and must maintain strict fiscal discipline, as it cannot finance deficits by printing money. Its economic fate is tied to Eurozone growth, particularly in Portugal. For this small, service-based archipelago, the benefits of ultra-low transaction costs, eliminated exchange rate risk for investors, and anchored inflation overwhelmingly justify the loss of policy autonomy, securing its place as one of Africa's most stable real currencies.

1. CFA Franc (XOF & XAF) Zones

Topping the ranking are the two CFA Franc zones, the West African Economic and Monetary Union (WAEMU) with the XOF and the Central African Economic and Monetary Community (CEMAC) with the XAF. Their stability is institutional and absolute: both currencies are pegged to the Euro, with a fixed, guaranteed convertibility rate. This peg is underwritten by the French Treasury, which holds the operating accounts of the zones' central banks. This arrangement completely eliminates nominal exchange rate risk against the Euro and imports the anti-inflation credibility of the European Central Bank, resulting in exceptionally low REER volatility.

The CFA Franc arrangement is the most potent mechanism for REER stability on the continent, but it is also the most politically debated. It provides a haven of monetary stability and low inflation for member countries, fostering regional integration and attracting long-term investment. However, it completely surrenders monetary sovereignty and can lead to periodic issues with external competitiveness, as the real exchange rate can become misaligned if inflation in the zone outpaces that of the Eurozone. Despite the political controversies, from a purely technical standpoint of Real Effective Exchange Rate stability, the guaranteed peg makes the CFA Francs the most stable currencies in Africa.

We welcome your feedback. Kindly direct any comments or observations regarding this article to our Editor-in-Chief at [email protected], with a copy to [email protected].

){kind=link}