![South Africa topped the 2025 ranking with the largest cumulative solar capacity. [Photo Credit: File]](/content/images/size/w1304/format/webp/2025/12/Solarise-Africa.jpg)

Table of Contents

In Summary:

- By mid-2025, Africa’s cumulative solar capacity exceeded 20GW, with more than 10GW under construction at the beginning of the year.

- In 2024 alone, the continent added 2.4–2.5 GW of new solar capacity; nearly 80% of those additions came from just two countries; South Africa and Egypt.

- Rapid growth in West Africa was evident as Ghana added 94 MW in 2024, while Nigeria added 63.5 MW, lifting both countries significantly in regional solar adoption rankings.

- Utility-scale PV now dominates new installations (about 70 % of capacity under construction), but distributed rooftop systems are expanding fast, offering access beyond urban centers.

Deep Dive!!

Tuesday, 09 December, 2024 – Africa’s solar energy landscape reached an important inflection point by 2025 as the continent pushed past 20 gigawatts of operational solar capacity. Data from the Africa Solar Industry Association and other trackers point to a remarkable surge in installations during 2024 and early 2025. Driven by falling panel costs, advancing grid infrastructure, and growing policy support, solar is no longer a niche option, it is rapidly becoming a central plank in many national energy strategies.

This transformation reflects more than just large utility-scale projects led by a few countries. A growing number of nations across the continent now feature robust solar pipelines, commercial rooftop growth, off-grid mini-grids and home-system deployment. That diversification is helping to broaden access, reduce reliance on fossil-fueled grids, and empower households, businesses and rural communities. As solar markets deepen and capital flows, the energy map of Africa is beginning to shift decisively.

In the sections that follow, we explore the top ten African solar markets in 2025, spotlighting countries that combine scale, growth momentum, supportive policy environments and strong project pipelines. The ranking draws on verified 2024–2025 data to show which nations are leading the charge and how solar energy is reshaping power generation and access across the continent.

10. Ghana

Ghana’s solar market grew materially in 2024/2025 as off-grid electrification programmes, commercial rooftop installations and utility-scale tenders all accelerated; IRENA statistics and project trackers show a clear uptick in small-to-medium PV capacity additions. Donor-backed mini-grid financing and pay-as-you-go residential systems helped reach rural populations while commercial rooftop uptake rose among retailers and telecoms seeking backup power. These distributed deployments reduced reliance on diesel generation and created a broad base for future utility-scale integration.

Regulatory adjustments in 2024 eased private-sector entry for independent power producers and simplified permitting for rooftop systems, which encouraged local developers and international investors to scale projects. Several medium-sized utility PV projects reached financial close in late 2024 and entered construction in 2025, strengthening Ghana’s pipeline and bringing grid-connected solar capacity online. The mix of donor finance and private capital has been pivotal in removing upfront cost barriers for smaller communities and enterprises.

Sector analysts note that Ghana’s combined approach, pairing large projects with pervasive distributed solutions, is reshaping its electricity mix. The market’s diversity supports resilience, because mini-grids and rooftop systems buttress the national grid during peak demand and reduce transmission losses in remote regions. Over the short term, these dynamics suggest continued steady capacity growth through 2025 and beyond.

9. Namibia

Namibia’s excellent solar irradiance and investor-friendly policy environment attracted meaningful utility and commercial PV activity in 2024/2025, lifting its installed base relative to population size. Large-scale commercial plants and corporate rooftop programmes reached advanced stages, with developer announcements and IRENA country notes documenting new capacity additions and commissioning activity. These projects directly target mining camps, industrial parks and water-pumping electrification, sectors that benefit from stable, low-cost solar power.

The government’s updated renewable framework and streamlined procurement mechanisms improved bankability for independent power producers, enabling a wave of private investment in mid-sized PV plants. Off-grid solar systems and agricultural solar pumps also expanded, supported by concessional finance and technical assistance that reduce unit installation costs for farmers and rural entrepreneurs. This combination of on-grid and off-grid growth helped Namibia progress up regional solar rankings in 2025.

Market observers emphasise that Namibia’s strategic focus on commercial-scale solar for industry and water services creates a durable demand anchor. By aligning solar development with industrial and water-security needs, the country has translated excellent solar resources into tangible projects that strengthen economic activity while advancing decarbonisation goals.

8. Ethiopia

Ethiopia advanced several utility-scale PV projects in 2024/2025 as part of its electrification and renewable diversification agenda, combining large grid-connected plants with aggressive rural solar programmes. Competitive tenders and international development finance supported project pipelines, and industry trackers recorded multiple utility PV agreements moving toward construction during 2025. Off-grid solutions remained central to rural electrification, with solar-home-system rollouts continuing to expand access.

Public–private partnerships became more common in Ethiopia’s solar deployment strategy, enabling developers to leverage government offtake guarantees and concessional finance to unlock larger projects. The integration of utility PV into the national system helped reduce the marginal cost of generation and complemented hydropower, which faces seasonality risks. Developers and DFIs cited Ethiopia’s scale potential as the reason for growing investor interest in the country’s solar programme.

Analysts observe that Ethiopia’s dual approach, expanding both grid-scale PV and decentralised solutions, strengthens long-term energy security. As new plants come online, the country is better positioned to meet industrial demand, lower power costs, and accelerate productive-use electrification across previously underserved regions.

7. Nigeria

Nigeria’s 2024/2025 solar activity was dominated by distributed adoption: commercial rooftops, pay-as-you-go household systems and an expanding mini-grid market collectively generated most new capacity additions. Market reports from Ember and project databases show a step-change in installations driven by rising demand from SMEs and telecom towers seeking reliable supply amid grid constraints. The large addressable market, combined with increased module imports, fuelled rapid deployment at multiple scales.

Financial innovation accelerated uptake, with pay-as-you-go models and blended financing lowering upfront barriers for low-income households and micro-businesses. Private-sector investors and development partners scaled funding lines for mini-grids and commercial rooftops, while regulatory pilots in some states tested streamlined interconnection and net-metering rules. These pilots improved project bankability and encouraged further private capital.

Looking ahead, Nigeria’s market structure, vast population centers plus large rural areas, means distributed solar will remain the short-term growth engine even as utility-scale projects advance. The country’s ability to link commercial deployment with selective utility tenders will determine whether Nigeria moves from rapid distributed growth to sustained, large-scale solar integration.

6. Tunisia

Tunisia continued to implement policy reforms in 2024/2025 that opened the market to private investment and sped up approval processes for mid-sized PV plants and rooftop projects. IRENA country briefings and national programme updates highlight steady additions in both distributed and utility categories, reflecting a maturing procurement environment and clearer tariff frameworks. These changes encouraged domestic and foreign developers to pursue commercially viable PV opportunities.

Rooftop adoption grew among industrial and commercial consumers seeking lower and more predictable energy costs, while utility tenders added competitive capacity to the system. The government’s renewable target roadmap and supportive grid-integration planning reduced technical bottlenecks for connecting new PV plants, improving overall market absorption capacity. Project pipelines indicated steady growth rather than abrupt expansion, aligning with Tunisia’s methodical policy-driven approach.

Market analysts note that Tunisia’s incremental and policy-led expansion helps balance grid stability with renewable integration. The country demonstrates how stable regulatory design and phased auctions can foster investor confidence and produce sustainable solar growth without destabilising electricity markets.

5. Algeria

Algeria’s national solar ambitions moved decisively from planning toward execution in 2024/2025, anchored by the government’s multi-gigawatt programmes and competitive tender activity. Official announcements and industry bulletins documented tender structuring and module procurement steps that signalled near-term capacity additions, positioning Algeria as a major North African market by pipeline volume. These programmes focus on utility clusters designed to accelerate energy transition and reduce fossil-fuel dependence.

Domestic and international contractors engaged in early-stage EPC and financing discussions, while the state coordinated grid reinforcement to receive large PV output. Algeria’s size and electricity demand profile make utility-scale solar particularly impactful, offering potential to free gas for export while meeting domestic power needs with low-carbon generation. Such macro considerations underlie investor interest in the country’s large-scale projects.

Observers emphasise that Algeria’s move from policy blueprint to execution, if sustained, will materially reshape its electricity mix. Successful procurement, strong project management and timely grid upgrades are critical to converting the country’s large pipeline into commercial capacity through 2025 and beyond.

4. Kenya

Kenya combined competitive utility tenders, corporate procurement and a thriving mini-grid sector to deliver robust solar capacity growth in 2024/2025; IRENA and regional trackers show substantial net additions in the period. The country’s experienced tender framework and supportive private-investor signals attracted international developers, while local entrepreneurs scaled commercial rooftop and off-grid solutions in parallel. This multi-track approach strengthened Kenya’s leadership across East Africa.

Commercial users, notably horticulture, manufacturing and telecoms, continued to sign power-purchase and self-generation agreements, driving demand for large rooftop and ground-mounted systems. Mini-grid and solar-home-system providers also scaled, backed by donor funds and impact investors focused on last-mile electrification. Core infrastructure investments in transmission and distribution improved interconnection prospects for new solar plants.

Industry analysts highlight that Kenya’s mature market institutions and regular auction cadence give it a sustained edge for solar growth. The country’s balance of centralized auctions and decentralised deployment enables a resilient and diversified solar market capable of meeting both urban industrial and rural electrification needs.

3. Morocco

Morocco’s solar maturity is evident in its combination of large-scale utility PV, concentrated solar power and integrated renewables planning; projects such as the Noor complex and multiple PV plants established the country as a regional pioneer by 2024. Industry sources and project trackers documented Morocco’s advanced pipeline entering 2025, with further auctions and hybrid projects reinforcing its renewable leadership. The established industrial cluster around Noor remains a strategic asset for larger regional ambitions.

Public policy and integrated planning enabled Morocco to combine CSP for storage needs with large PV zones, attracting long-term project finance and technical partnerships. Manufacturing linkages and industrial park synergies improved the local value chain for solar deployment, helping reduce costs and strengthen supply security for major projects. This institutional depth differentiates Morocco from many emerging markets.

Sector commentary notes that Morocco’s success stems from deliberate sequencing of technology mixes and industrial engagement. By pairing utility-scale deployment with manufacturing and storage-focused projects, Morocco maintained high pipeline quality and delivered material capacity additions through 2025.

2. Egypt

Egypt’s large utility clusters, most prominently the Benban solar complex, continued to anchor its standing as a continental solar heavyweight in 2024/2025; Benban alone represents a multi-gigawatt deployment that reshaped North African solar capacity statistics. Additional tenders and Red Sea project announcements in 2024/2025 expanded the country’s near-term pipeline, reinforcing Egypt’s role as a major recipient of project investment and developer activity. Government procurement frameworks and grid planning supported these rapid additions.

Industrial demand, especially from energy-intensive sectors and export-oriented manufacturing, provided a strong commercial rationale for expanded solar deployment. The scale of utility projects allowed Egypt to leverage economies of scale in procurement and to attract cross-border investors focused on large, bankable assets. This scale advantage distinguishes Egypt’s market dynamics from smaller regional markets.

Energy analysts highlight that Egypt’s combination of large projects, active auction programmes and integrated grid upgrades positioned it to absorb substantial variable renewable energy while supporting industrialisation goals. As projects commissioned through 2025, Egypt consolidated its position as the continent’s second-largest solar market by installed utility PV capacity.

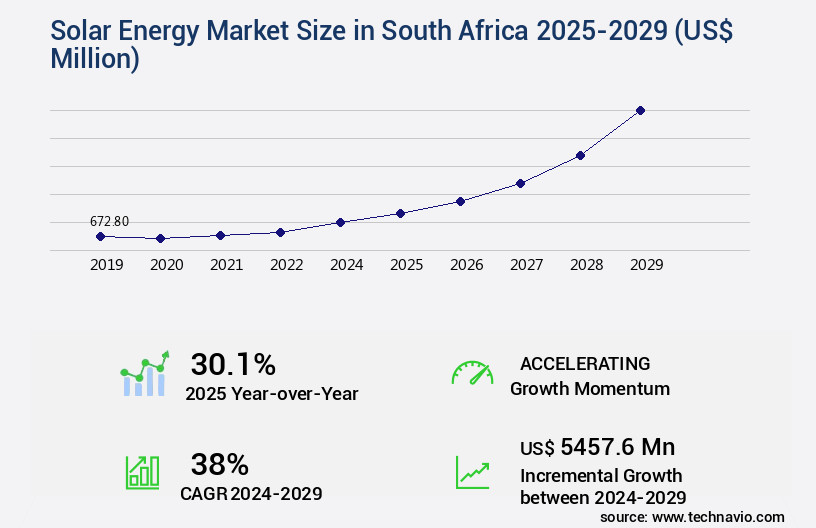

1. South Africa

South Africa topped the 2025 ranking with the largest cumulative solar capacity and the deepest commercial pipeline, combining successful utility auctions, a mature commercial rooftop segment and accelerating private deployment. IRENA, IEA and multiple industry trackers recorded South Africa as the only African market approaching multiple gigawatts of cumulative PV by the 2024/2025 cycle, with continued build-out under the Renewable Energy Independent Power Producer Procurement Programme and corporate procurement schemes.

The country’s commercial industrial base, large mining, manufacturing and services sectors, created robust demand for both on-site generation and contracted utility-scale supply. Project bankability improved with established legal frameworks, and a growing community of EPC contractors and financiers supported rapid deployment. At the same time, distributed energy resource integration, storage pilots, and corporate offtake deals increased market sophistication.

Analysts emphasise that South Africa’s combination of scale, institutional maturity and private-sector appetite makes it the continent’s solar market benchmark in 2025. Continued auction cycles, improvements in grid flexibility and rising corporate demand are expected to sustain South Africa’s lead as developers deliver further gigawatts of PV in the medium term.

We welcome your feedback. Kindly direct any comments or observations regarding this article to our Editor-in-Chief at[email protected], with a copy to[email protected].

{kind=link}