Table of Contents

In Summary:

- African forex reserve growth in 2025 was driven largely by improved oil and gas receipts, stronger commodity exports, and disciplined central bank policies.

- Countries like Libya, Algeria, and Nigeria recorded sharp reserve increases due to energy price stability and higher export volumes.

- Diversification into gold, agriculture, and services boosted reserve positions for nations such as Ghana, Morocco, and Rwanda.

- Rising reserves strengthened currencies, improved investor confidence, and enhanced countries’ ability to manage debt and external shocks.

Deep Dive!!

Saturday, 13 December 2025 – Africa’s foreign exchange reserves are a critical indicator of economic resilience, external stability, and policy credibility. In 2025, several African countries recorded notable growth in their forex reserves, driven by a mix of higher commodity exports, improved fiscal discipline, external financing inflows, and stronger monetary management. Tracking reserve growth, rather than absolute size, provides deeper insight into how economies are strengthening buffers against currency shocks, inflationary pressures, and global financial volatility.

This article ranks the top 10 African countries with the highest forex reserves growth in 2025, using verified data and analysis from credible institutions such as central banks, the IMF, World Bank, and international financial reports. By examining the underlying drivers behind each country’s performance, the ranking highlights emerging success stories, policy lessons, and structural trends shaping Africa’s evolving macroeconomic landscape.

10. Tanzania

Tanzania’s foreign exchange reserve growth in 2025 reflected a steady strengthening of its external position rather than a one off surge. Bank of Tanzania disclosures showed reserves consistently exceeding five months of import cover, a level widely viewed by the IMF as a sign of external stability for emerging economies. This performance was anchored by sustained gold exports, which remain Tanzania’s largest foreign exchange earner.

Tourism also played a material role in reserve accumulation. Official tourism receipts rebounded strongly following expanded international arrivals to Serengeti, Zanzibar, and Ngorongoro, with World Bank updates noting improved service export inflows during the year. These inflows helped offset pressures from fuel and capital goods imports, allowing net reserves to trend upward.

Monetary coordination and cautious external borrowing further supported reserve growth. The central bank limited excessive FX intervention while smoothing volatility, which helped preserve reserves. As a result, Tanzania entered late 2025 with improved investor confidence and stronger buffers than several regional peers.

9. Botswana

Botswana’s reserve growth in 2025 marked a recovery phase following a dip in late 2024. Bank of Botswana bulletins showed a gradual rebound driven by improved diamond export receipts as global demand stabilized and sales volumes recovered from earlier softness.

Fiscal restraint also contributed to rebuilding buffers. Government spending discipline limited drawdowns on foreign assets, while sovereign wealth management through the Pula Fund allowed for a measured accumulation of reserves. CEIC data confirmed a positive quarter on quarter trend through early and mid 2025.

Although Botswana’s reserves remain modest in absolute dollar terms compared with larger African economies, the percentage growth in 2025 was notable. This rebound reinforced Botswana’s reputation for prudent macroeconomic management and strong institutional credibility.

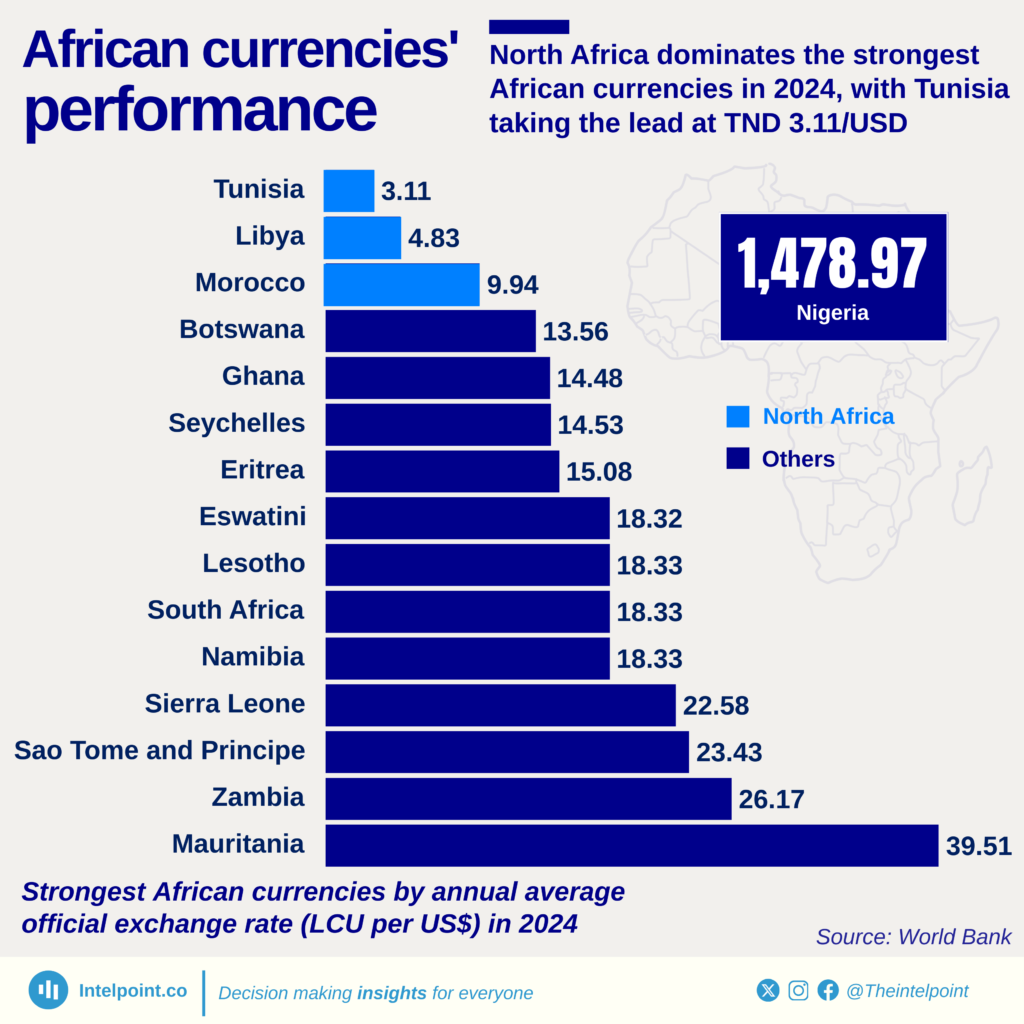

8. Tunisia

Tunisia’s foreign exchange reserves showed intermittent but meaningful recovery during 2025 after prolonged pressure in prior years. Central Bank of Tunisia bulletins documented month to month increases during mid 2025, reflecting improved inflows from tourism and remittances.

TradingEconomics and CEIC time series showed reserves gradually improving import cover, easing concerns about short term external financing gaps. Domestic media reports confirmed that net FX buffers rose again toward the final quarter of 2025, helping stabilize currency expectations.

Despite these gains, Tunisia’s reserve position remained fragile relative to historical norms. However, the positive direction of movement in 2025 represented a clear break from the sharp declines seen earlier, signaling incremental progress in restoring external balance.

7. Kenya

Kenya’s forex reserve growth in 2025 was underpinned by diversified inflows rather than commodity dependence. Central Bank of Kenya weekly bulletins showed reserves comfortably above IMF program thresholds, supported by strong diaspora remittances and resilient tea and horticulture exports.

Improved external financing conditions also played a role. Ratings agencies and IMF commentary cited Kenya’s reserve accumulation as a factor behind enhanced market confidence, including a credit outlook improvement in August 2025. This helped stabilize the shilling and reduce speculative pressure.

By maintaining consistent reserve build up throughout the year, Kenya strengthened its capacity to manage external shocks. The accumulation reflected structural resilience rather than short term inflows, reinforcing its standing as one of East Africa’s financial anchors.

6. Algeria

Algeria’s reserve performance in 2025 benefited primarily from hydrocarbon revenues. IMF reporting highlighted higher gas and oil receipts as a major contributor to improved external buffers, allowing the central bank to rebuild reserves after earlier drawdowns.

National statistics showed reserves remained among the largest in Africa, with monthly fluctuations reflecting global energy prices rather than domestic instability. The net effect over 2025 was a strengthening of Algeria’s reserve position compared with near term pressures in prior years.

Policy emphasis on buffer rebuilding also mattered. Authorities limited fiscal expansion and prioritized external stability, helping Algeria preserve its foreign assets and maintain significant import cover.

5. Morocco

Morocco’s reserve growth in 2025 was steady and policy driven. Bank Al Maghrib data and CEIC series showed net international reserves trending upward through the year, reaching roughly forty one billion US dollars by October 2025.

Tourism was a key driver, with record visitor numbers generating strong service export receipts. At the same time, export performance in automotive and phosphates supported foreign currency inflows, easing balance of payments pressures.

The central bank’s cautious intervention strategy allowed reserves to accumulate without excessive currency volatility. This combination of diversified exports and disciplined monetary policy positioned Morocco among Africa’s more stable reserve builders in 2025.

4. Egypt

Egypt recorded a visible and sustained rebuild of reserves during 2025. Central Bank of Egypt releases showed net international reserves exceeding fifty billion US dollars by October and November, reflecting a clear upward trajectory.

Tourism revenues recovered strongly, while Suez Canal related receipts and official financing inflows supported foreign exchange availability. These inflows helped offset import demand and external debt servicing pressures.

Although Egypt continues to face structural external challenges, the scale and consistency of reserve accumulation in 2025 marked a significant improvement from earlier volatility, restoring confidence in near term liquidity.

3. South Africa

South Africa’s reserve growth in 2025 was modest in percentage terms but significant in absolute value. South African Reserve Bank data showed net reserves rising from approximately sixty five point nine billion US dollars in August to about sixty seven point nine billion by late September.

Improved current account dynamics and portfolio inflows supported this accumulation. Reuters reporting linked reserve gains to better export receipts and stabilizing financial flows amid improved global risk sentiment.

As Africa’s most industrialized economy, South Africa’s reserve increase reinforced its ability to manage currency volatility and external shocks, maintaining one of the continent’s largest liquidity buffers.

2. Ghana

Ghana experienced one of Africa’s most dramatic reserve recoveries in 2025. Reuters and Bank of Ghana statements attributed the rebound largely to the launch of a state run gold trading program that redirected export proceeds into official reserves.

Diaspora remittances and fiscal consolidation under IMF supported reforms also strengthened external buffers. Import cover improved markedly compared with the crisis years of 2022 and 2023, restoring short term liquidity confidence.

The speed and scale of Ghana’s reserve growth in 2025 stood out continent wide, positioning the country as a leading example of post crisis recovery driven by structural policy shifts.

1. Nigeria

Nigeria recorded the largest absolute increase in foreign exchange reserves in Africa during 2025. Reuters and Central Bank of Nigeria disclosures documented a multibillion dollar rise driven by higher oil export receipts, improved FX market reforms, and reduced short term liabilities.

The central bank’s strategy of clearing FX backlogs and limiting unproductive interventions allowed reserves to rebuild steadily across 2024 and 2025. By late 2025, gross external reserves were reported at their highest levels in several years.

Nigeria’s reserve growth reflected both improved external earnings and policy credibility. In scale, pace, and continental impact, Nigeria’s 2025 reserve accumulation ranked unmatched across Africa.

We welcome your feedback. Kindly direct any comments or observations regarding this article to our Editor-in-Chief at [email protected], with a copy to [email protected].

{kind=link}