Table of Contents

For an investor or operator setting up a delivery centre, a fintech product, or a regional engineering team in Sub‑Saharan Africa, talent determines how quickly teams can be hired, how systems are built, and whether operations can scale without disruption.

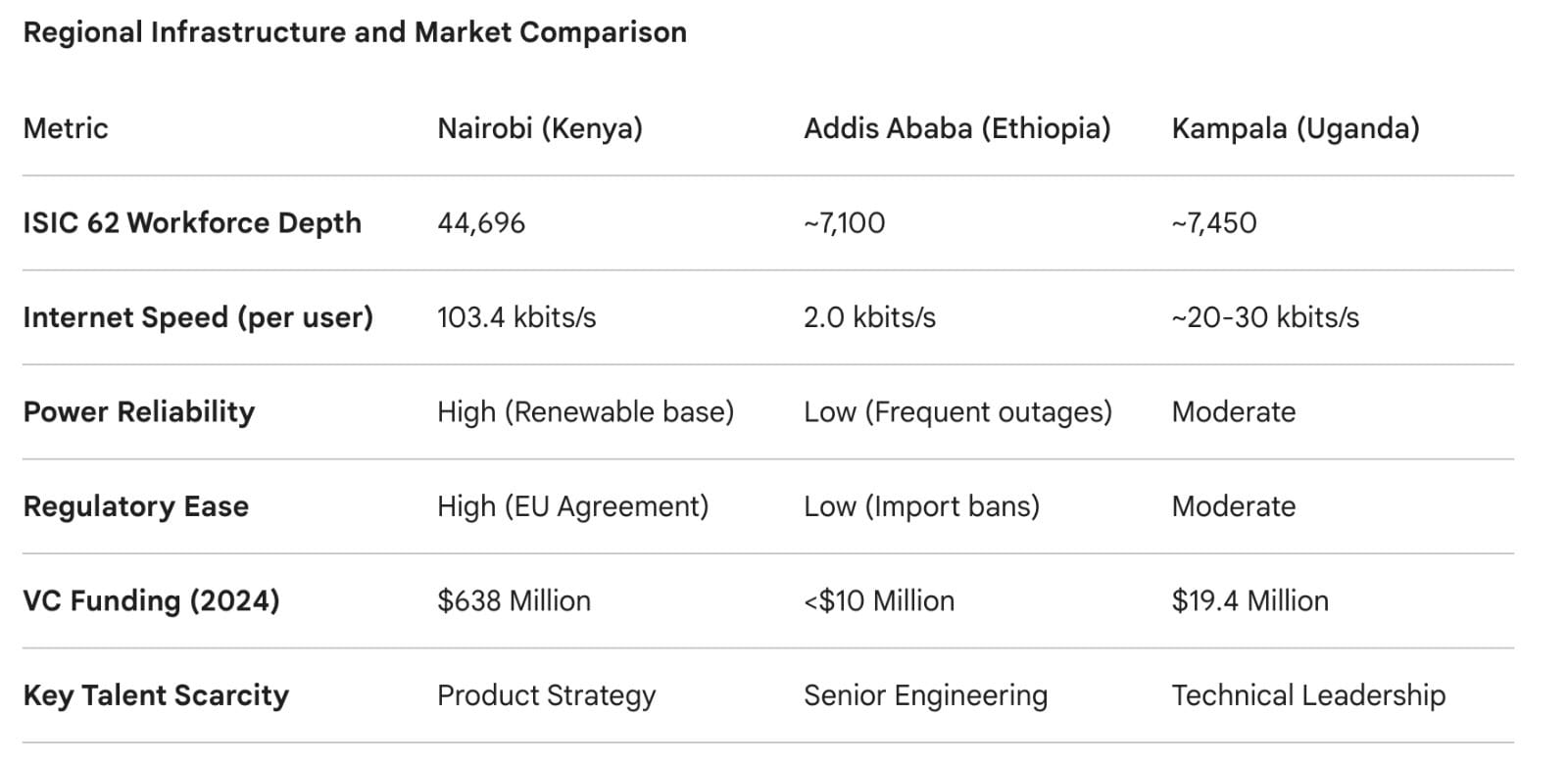

This is where Kenya stands out. According to the International Labour Organization’s database, Kenya had 44,696 workers in computer programming, consultancy, and related activities as of 2022, the largest count among African countries surveyed by the ILO.

On its own, that suggests a clear advantage. A workforce of that size should support faster hiring, deeper specialization, and the ability to build large teams without exhausting the talent pool.

But scale at this level does not operate in only one direction. A labour market of this size influences wage growth, increases movement between firms, and shapes how long employees stay within a single role. What looks like depth on paper can, in practice, behave very differently depending on how demand interacts with that supply.

So the question is not whether Kenya has the largest software workforce in the region. It is what that workforce actually enables companies to build, how stable those advantages are over time, and where the limits begin to show.

What Does Kenya’s Software Workforce Actually Enable for Companies Building Tech Operations in Africa?

For companies deciding where to build technology teams, workforce size only matters if it translates into real operating capacity. In Kenya’s case, that capacity becomes visible through how global and regional firms have structured their presence in Nairobi.

When Microsoft launched its Africa Development Center (ADC) in 2019, it chose Nairobi as one of its key engineering hubs, signalling confidence in the ability to hire local software engineers and data scientists at scale. Microsoft ADC Nairobi is now an established engineering base working on major products and solutions, not just outsourced tasks.

This ability to support full engineering operations is reinforced by the broader ecosystem. Google has an engineering and product presence in Nairobi, and Amazon Web Services (AWS) actively promotes its cloud services infrastructure across East Africa with local technical teams. These are operational bases that rely on locally hired engineers, product managers, and technical specialists.

What these point to is not just availability, but functional depth. Kenya’s tech workforce supports multiple layers of technical roles at the same time, allowing companies to move beyond basic development into structured product teams and complex engineering operations.

This depth is visible even in local platforms such as M‑Pesa, Kenya’s mobile money service originally developed by Safaricom and Vodafone. M‑Pesa has been used by tens of millions of people in Kenya and beyond, and while official figures for total processed transaction values vary, other reporting estimates have placed valuations in the hundreds of billions of dollars range in terms of overall transaction value over time.

At the ecosystem level, this concentration of talent allows multiple companies to operate simultaneously without immediately exhausting the labour pool. In 2025, African tech startups raised more than US$4 billion in combined equity and debt financing, with Kenya ranking among the top countries both in deal winners and capital raised (US$1.04 billion of that total).

Taken together, what the workforce enables is not just the presence of tech companies, but the ability to build, run, and expand complex operations within a single market. Companies can establish engineering hubs, support large‑scale platforms, and operate alongside other talent‑intensive firms because the underlying workforce is deep enough to sustain multiple layers of demand at once.

Is Nairobi’s Tech Talent Pool Showing Signs of Strain, or Can It Absorb Growing Demand?

The Nairobi technology ecosystem faces competitive pressure as companies vie for highly skilled talent. Salary benchmarks show that mid‑level software developers in Nairobi typically earn between roughly KES 250,000 and KES 275,000 per month (approximately US$160–US$175, based on recent exchange rates), while senior developers often earn significantly more.

Specialized roles such as machine learning engineers, cloud architects, and data scientists attract higher compensation due to limited supply and strong demand, as seen in regional salary surveys.

Recruitment trends also highlight mobility pressures. Kenyan tech talent frequently moves between employers, startups, and large firms, and often pursues better pay or growth opportunities, creating talent churn and retention challenges.

Beyond full‑time employment, a notable portion of Kenya’s tech workforce engages in freelance or contract roles. While exact aggregate figures vary across sources, surveys, and market observations confirm that freelance work constitutes a substantial segment of the ecosystem.

Comparisons with regional peers further underscore Nairobi’s centrality and the strain it places on it. Kenya’s tech workforce (44,696) stands significantly larger than the broader employment footprints reported for tech‑related roles in countries like Uganda and Ethiopia, where employment for similar roles is much lower based on ILO estimates.

In niche technology sectors such as AI, data engineering, and cloud architecture, firms report difficulty filling senior positions even as junior developers are more abundant, highlighting a skills gap at mid‑senior levels that companies must actively manage.

Together, these indicators show that while Nairobi’s tech talent pool is substantial, it is under measurable pressure in areas of high demand, specialized skillsets, and retention. Firms must plan for rising wage pressure, mobility of key staff, and competition for mid‑ and senior‑level expertise.

What Does Kenya’s Large Male Tech Workforce Mean for Companies Building Balanced Teams?

Kenya’s tech workforce is significantly male-dominated. Available data shows that women hold fewer than 30% of ICT roles in the country, reflecting a broader gender gap across Africa’s technology sector. ILO estimates suggest that for programming roles specifically, female representation drops to around 3%, highlighting a much wider disparity within core technical functions.

This imbalance is linked to pipeline constraints in education and early career entry, where female participation in ICT training and degree programs remains low.

This structural imbalance is relevant for organisations aiming to build balanced teams. Broader trends in STEM participation show that female representation in technical and engineering fields is generally lower than male participation, in part due to pipeline issues in education and early career entry points.

For employers, this means that deliberate recruitment and retention strategies such as partnerships with female‑focused coding programmes, targeted mentorship schemes, and inclusive workplace policies are essential to achieving gender balance. Without such interventions, companies cannot rely solely on the existing local labour market to yield balanced teams.

When Should You Choose Nairobi Over Addis Ababa or Kampala for Tech Operations, and What This Means for Investors

Nairobi remains East Africa’s most developed and specialised tech hub, anchored by its 44,696‑strong software and tech workforce. This concentration supports a wide range of functions, making it suitable for complex, multi‑layered tech operations.

For investors, this workforce depth is critical. The concentration of engineers and technical talent enables rapid scaling, supports diverse functional roles, and provides a consistent pipeline of skills needed for advanced technology projects.

By contrast, countries like Ethiopia and Uganda have smaller formal tech workforce bases. ILO estimates show that Ethiopia has about 7,739 programmers and Uganda about 7,687, compared to Kenya’s 44,696, highlighting a significant gap in both scale and depth.

Investors looking to pilot smaller operations such as focused coding teams or niche support functions may find these markets cost‑effective and less subject to wage competition than Nairobi, though they lack the broader talent depth required for full‑scale engineering hubs.

Nairobi’s larger pool also creates wage competition and higher churn, particularly among mid‑ and senior‑level developers, and investors should weigh the trade‑off between talent access and retention challenges.

Structural factors like the male‑dominated workforce also influence hiring strategies and inclusion goals, especially for firms with global diversity commitments.

Beyond talent numbers, Nairobi’s ecosystem offers additional advantages through accelerators, coding academies, and networking hubs that help maintain a pipeline of skilled workers and ongoing upskilling opportunities. These features make Nairobi attractive for long‑term, scalable technology operations compared with smaller regional markets.

Nairobi is the preferred location for operations demanding scale, specialization, and advanced technical skills, while Addis Ababa and Kampala may suit smaller, cost‑sensitive projects. Decisions should weigh workforce depth, function complexity, retention risk, and inclusion goals making Nairobi the strategic choice for long‑term growth in East Africa.