Table of Contents

Across Africa, governments are beginning to rethink the regulatory foundations of the gig economy as platform work expands across ride-hailing, delivery, and digital freelancing markets. Labour reforms aimed at extending protections such as pensions, health insurance, and workplace safety to gig workers could fundamentally reshape the unit economics of flexible contractor labour models that platforms like Uber, Bolt, and Glovo have built their growth strategies around.

Kenya has emerged as one of Africa’s most closely watched test cases, where a cluster of policy initiatives, such as the proposed Labour Laws Amendment Bill and reforms, align with discussions at the International Labour Organisation. If implemented, the reforms could improve gig workers' benefits, but also add statutory labour costs that may force companies and investors to rethink their operating models. Whether the shift ultimately strengthens the sustainability of digital labour markets or slows platform innovation will depend on how Kenya balances worker rights with the economics of the continent’s rapidly growing platform economy.

Why is the Spotlight on Kenya?

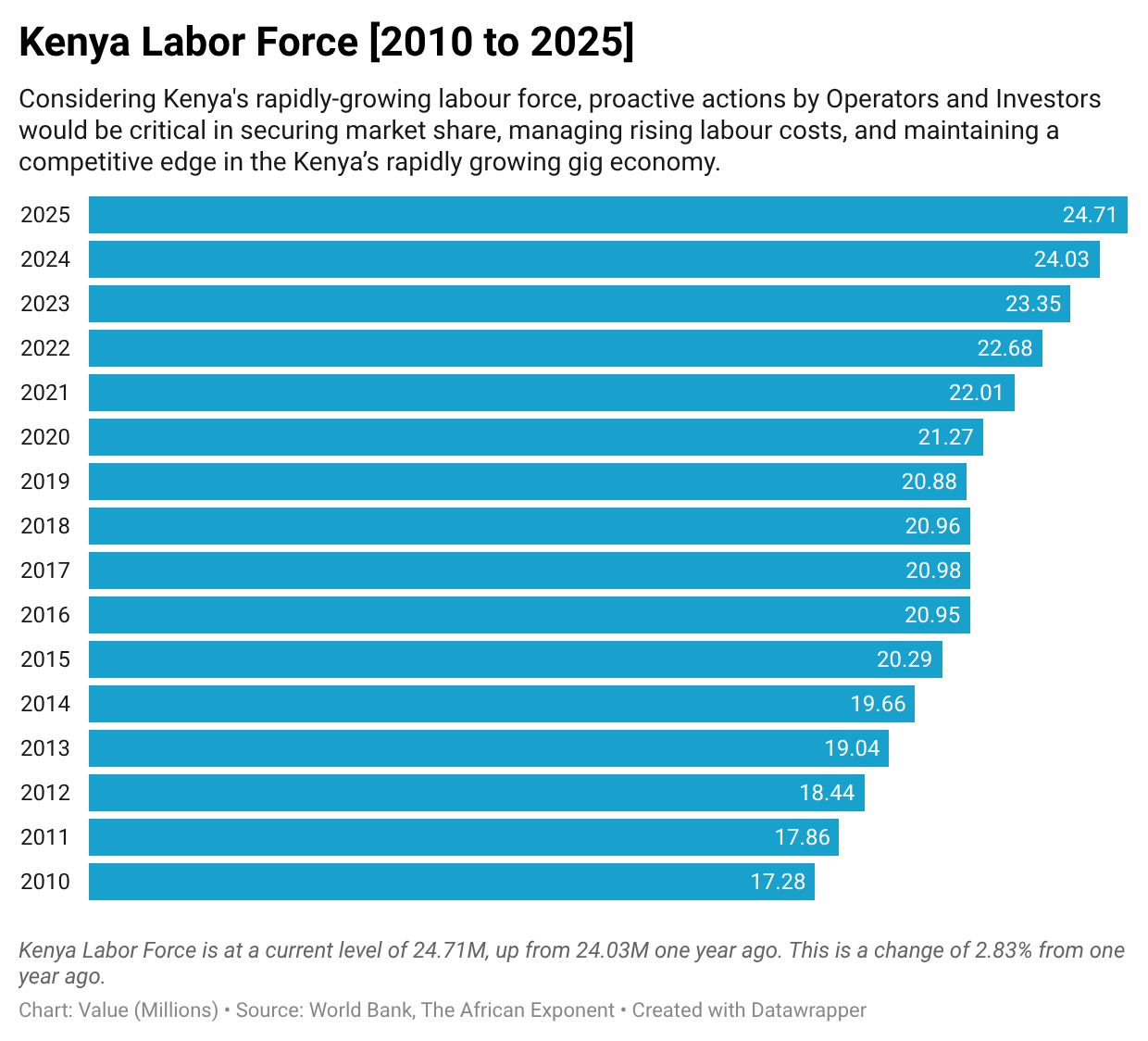

Kenya’s fast-growing gig economy has become one of the most visible examples of digital labour markets in Africa. Platforms such as Uber, Bolt, and Glovo have created new earning opportunities for approximately 1.2 million to over 1.5 million people, accounting for roughly 4.7% of the total Kenyan workforce.

However, the labour model underpinning these platforms is now under scrutiny. Kenya is considering regulatory changes that could reclassify gig workers, including drivers, couriers, and freelancers, as workers.

Although there is no direct gig/digital labour law proposal currently being proposed in the country, several policy initiatives are converging in that direction. The policies are included in the proposed Labour Laws Amendment Bill, Kenya’s National BPO Policy (2025), and global labour policy discussions led by the International Labour Organization, which Kenya and many other African countries are following closely. If implemented in Kenya, there is a high chance that the labour reforms would be adopted across the continent.

What is the Current Structure of Kenya’s Platform Economy?

Kenya’s gig economy has grown rapidly over the past decade, driven by rising smartphone adoption, widespread mobile payments, and persistent youth unemployment. Gig platforms have helped fill a major employment gap by enabling flexible work in transport, delivery, and digital freelancing. Estimates suggest about 1.5 million Kenyans now earn income through digital platforms, with tens of thousands of ride-hailing drivers operating across multiple apps in Nairobi alone.

Ride-hailing and delivery remain the most visible parts of the platform economy because they depend on large numbers of physical workers. Drivers and couriers typically operate as independent contractors, supplying their own vehicles or motorcycles, covering expenses such as fuel and maintenance, and earning per trip or delivery. This structure allows platforms to scale quickly while keeping labour costs variable, but it also means workers often lack the social protections associated with formal employment.

Research by Fairwork shows most digital labour platforms studied were unable to demonstrate that workers consistently earned at least the local minimum wage once work-related costs such as fuel and vehicle maintenance were considered. The assessment found that only one platform—Glovo—could provide evidence that workers did not fall below the minimum wage after these expenses, highlighting broader concerns about pay transparency and income security for gig workers in the country.

What Does the Policy Shift from Contractor to Employee Entail?

The proposed Labour Laws Amendment Bill is one of the most significant initiatives under discussion that would affect the labour reforms in the country. Under the Bill, the legislation extends key employment protections to certain categories of digital platform workers, potentially classifying them as employees or “dependent contractors” if they rely heavily on a platform for income.

Alongside this effort, Kenya’s National BPO Policy (2025) proposes a “Decent Work Toolkit” designed to improve labour standards across the outsourcing and digital services sectors. Meanwhile, international discussions led by the International Labour Organization are exploring global standards for platform work, with Kenya frequently referenced as a case study because of the country’s active digital labour market.

If these policy directions translate into legislation, platforms operating in Kenya could be required to provide or contribute to a range of statutory benefits that traditional employers already provide. These include:

- pension contributions through the National Social Security Fund

- health insurance contributions under the Social Health Insurance Fund

- and coverage for workplace injuries or occupational hazards.

Under Kenya’s pension rules, employers must contribute 6% of an employee’s pensionable earnings, which is matched by an employee contribution of the same amount. Health insurance contributions under the new system are set at 2.75% of gross income. For companies that currently treat labour purely as contractor payments, these obligations could introduce a new layer of payroll costs.

Who Is Most Exposed — and By How Much?

Platforms most exposed to labour reforms are those that depend on large pools of drivers or couriers, where labour represents the single largest operational cost. Ride-hailing companies such as Uber and Bolt operate extensive driver networks across Nairobi and other major Kenyan cities, with between 30,000 and 50,000 drivers estimated to be active in the capital alone. If reforms reclassify most drivers as employees or dependent workers, platforms could face labour cost increases of roughly 10–11% from statutory employer contributions alone.

For example, a typical driver earning KSh 70,000 (US$542) per month currently receives no employer pension or health contributions. If statutory payments become mandatory, platforms would need to contribute about KSh 4,200 (US$32.52) in pension payments and KSh 1,925 (US$14.91) in health insurance, adding roughly KSh 6,125 (US$47.43) in monthly labour costs per worker—an increase of nearly 9% before compliance or administrative costs. At scale, the impact is significant: a platform with 30,000 drivers could face additional payroll obligations exceeding KSh 2 billion (US$15,485,869.14) annually, depending on income levels and regulatory interpretation.

Another potential shift involves tax obligations for gig workers. If reforms formalise platform work or tighten enforcement around contractor income, drivers and couriers may increasingly fall within the tax net of the Kenya Revenue Authority. Many currently operate in a grey area with uneven tax compliance, but formalisation could require income tax declarations, social security contributions, or platform-linked withholding. While this could expand Kenya’s tax base, higher deductions may discourage some workers from joining or staying on platforms, particularly in ride-hailing and delivery where workers already cover costs such as fuel and vehicle maintenance. For platforms, this creates a second-order risk: if taxation reduces the attractiveness of gig work, labour supply could tighten, raising driver acquisition costs and potentially affecting service availability.

Food delivery and logistics platforms face similar exposure; companies such as Glovo rely on large networks of motorcycle couriers who operate as independent contractors and already absorb costs such as fuel, vehicle maintenance, mobile data, and insurance. If regulations require these couriers to be treated as workers, platforms may need to absorb some of these costs or guarantee minimum earnings—changes that could significantly affect profitability in a sector already operating on thin margins.

By contrast, online freelance marketplaces may face lower exposure. Platforms that connect Kenyan freelancers with international clients in fields such as software development or digital services typically operate as marketplaces rather than employers. If Kenya adopts a “functional dependency” test, only freelancers who rely heavily on a single platform for income would qualify for worker protections, limiting the number of workers captured by the regulation.

The Capital Markets Perspective: Why Investors Should Care

For investors and lenders, labour regulation represents a significant and historically underpriced risk in emerging markets. Authoritative market forecasts show that Kenya’s ride-hailing market revenue is projected to reach about $56.69 million in 2025 and grow to about $71.61 million by 2030, with an annual growth rate of roughly 4.79%. The sector’s rapid expansion, however, relies heavily on a labour model that treats drivers as independent contractors rather than employees.

This contractor-based model allows platforms to maintain flexible cost structures, where labour expenses scale directly with demand. If regulatory reforms reclassify gig workers as employees or dependent contractors, these economics could shift quickly, increasing labour costs and operational obligations.

Investors evaluating gig platforms will need to reassess several key metrics, including contribution margins per ride or delivery, the cost of retaining drivers and couriers under new labour rules, and the operational overhead associated with compliance and payroll management. Platforms that have not modelled these scenarios risk sudden margin compression and potential challenges to profitability.

Who Wins — and Why?

For many observers, the most immediate beneficiaries of labour reform are the gig workers—but this is not entirely the case. While it is true that many gig workers currently operate without retirement savings, formal health insurance, or income protection; and mandatory employer contributions to the National Social Security Fund and Social Health Insurance Fund could improve financial stability and reduce exposure to sudden income shocks, the benefits come with trade-offs.

Higher statutory labour costs could push platforms to reduce the size of their driver or courier networks, increase commissions, or tighten hiring standards to protect margins. In practice, this could mean fewer gig opportunities in the short term as workers become more expensive to onboard and retain.

Also, traditional employers may benefit from this shift. Logistics companies, courier services, and taxi cooperatives that already comply with labour regulations currently compete with digital platforms that operate with lower labour costs. If labour standards are harmonised, that cost advantage could narrow, helping level the playing field.

A third potential winner could be platforms that move early on compliance may also gain an edge. Companies that introduce benefits such as insurance, safety protections, or pension contributions ahead of regulation may find it easier to retain workers, attract institutional investors, and build stronger relationships with regulators.

In markets such as Europe and the United Kingdom, early compliance with gig worker protections has increasingly become a competitive advantage rather than simply a regulatory obligation. A notable example is Just Eat Takeaway, which shifted away from the contractor-only model and began hiring thousands of delivery couriers as employees in several European markets following court rulings and regulatory pressure. By offering formal employment contracts, guaranteed hourly wages, and benefits such as insurance and paid leave, the company positioned itself as a more worker-friendly alternative to rivals that continued relying solely on gig contracts. Analysts noted that this approach helped Just Eat strengthen courier retention, reduce labour disputes, and build stronger relationships with regulators in countries tightening platform labour rules.

What Happens Next: What Should Operators and Investors Do?

For platform companies planning their 2026 financial strategies, the direction of policy travel is already clear enough to require scenario planning. Waiting until legislation is formally enacted could leave operators scrambling to adapt their business models.

Kenya’s gig economy will likely continue to grow as digital services expand across Africa’s largest technology hubs. But if labour reforms proceed as expected, the cost structure of platform work will change, and companies that fail to anticipate that shift may find their margins squeezed.

{kind=link}