Table of Contents

From Resource Extraction to Energy Transition

China’s role in Africa’s energy sector has undergone a quiet but consequential transformation over the past two decades. In the early 2000s, Chinese financing and construction activity on the continent was overwhelmingly focused on fossil fuels, large hydropower dams, and transport infrastructure designed to move commodities. Coal-fired power plants, oil pipelines, and mining-linked infrastructure dominated early project portfolios, reflecting both Africa’s urgent power deficits and China’s own development trajectory at the time.

This approach began to shift in the early 2010s, driven by a convergence of forces. Africa’s electricity demand was rising faster than grid expansion, climate finance was becoming central to development discourse, and China itself was emerging as the world’s largest producer of renewable energy technologies. By 2013, when President Xi Jinping launched the Belt and Road Initiative (BRI), renewable energy had already become a strategic export sector for Chinese firms. Africa, with its vast solar, wind, hydro, and geothermal potential, increasingly became part of that equation.

The turning point came after 2015, when three developments aligned. First, the Paris Climate Agreement reframed energy investment globally. Second, African governments began prioritizing energy diversification and climate resilience in national development plans. Third, China’s policy banks and state-owned enterprises faced growing pressure to reduce exposure to coal projects overseas. Together, these forces laid the groundwork for a new phase of China–Africa engagement one centred less on extraction and more on energy transition.

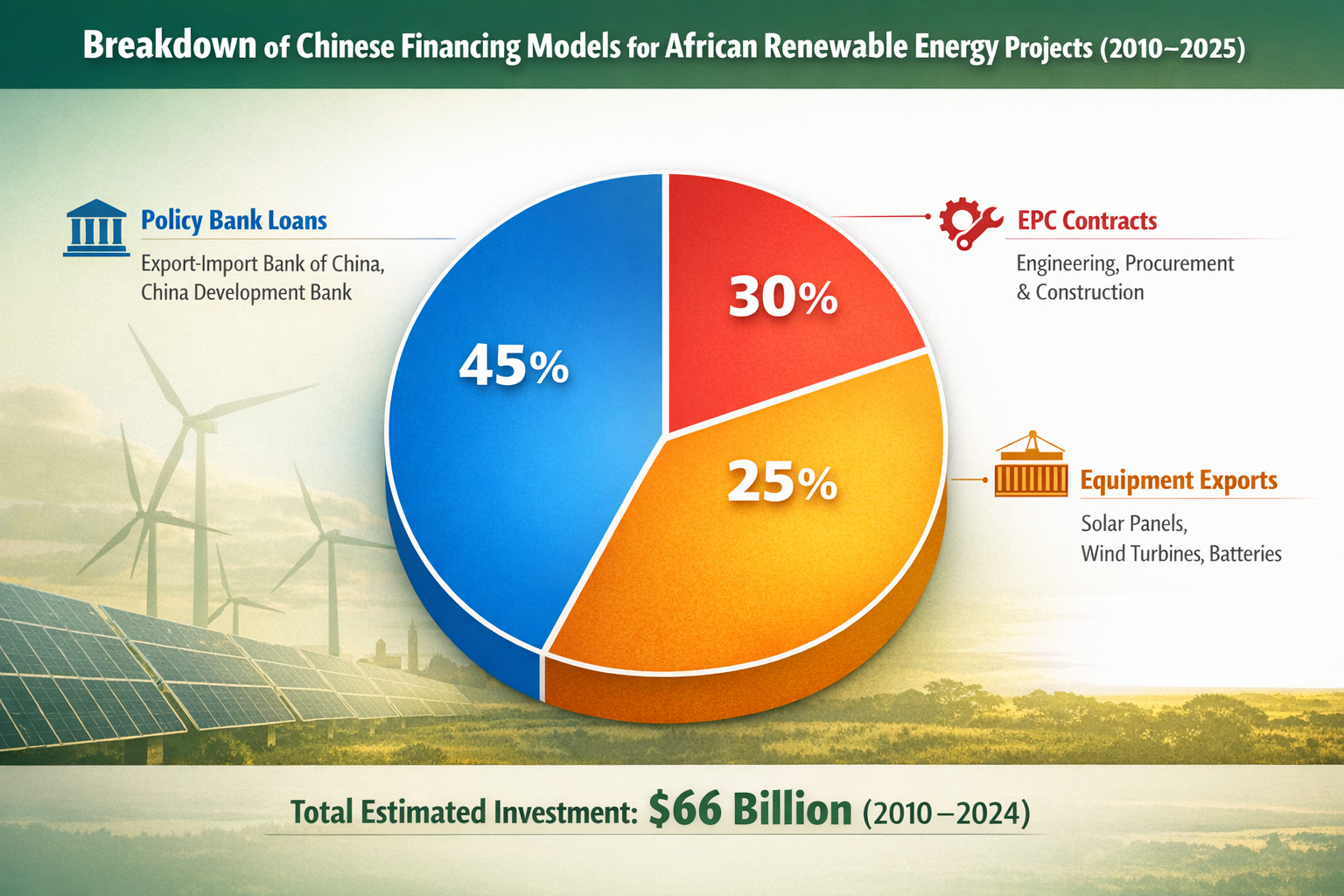

Breakdown of Chinese Financing Models for African Renewable Energy Projects (2010–2025). Data reflects estimated $66 billion in investments via policy bank loans, EPC contracts, and equipment exports. Source: UNCTAD, China Development Bank, African Development Bank

FOCAC and the Policy Architecture Behind China’s Green Push

The Forum on China–Africa Cooperation (FOCAC) has been the primary institutional platform shaping this shift. Since its launch in 2000, FOCAC has evolved from a trade-and-aid forum into a vehicle for strategic economic alignment. Renewable energy entered the agenda gradually but decisively.

At the 2015 Johannesburg FOCAC Summit, China formally committed to supporting African clean energy development under its “Ten Cooperation Plans.” This marked the first time renewables were framed as a standalone cooperation pillar rather than a subset of infrastructure. By the 2018 Beijing FOCAC Summit, clean energy had moved further up the agenda, with pledges for solar, wind, and hydro projects alongside capacity-building and technology transfer.

The most significant shift came at the 2021 Dakar FOCAC Ministerial Conference, where President Xi announced that China would stop building new coal-fired power plants overseas. While not Africa-specific, the implications for the continent were immediate. Financing and construction pipelines pivoted toward renewables, particularly utility-scale solar, wind farms, and grid-linked hydropower rehabilitation projects.

FOCAC 2024 further consolidated this direction, embedding green development within China–Africa cooperation frameworks through commitments to green finance, local manufacturing of renewable components, and skills transfer. Rather than isolated projects, Chinese renewable investments increasingly reflected longer-term strategic positioning within Africa’s energy transition.

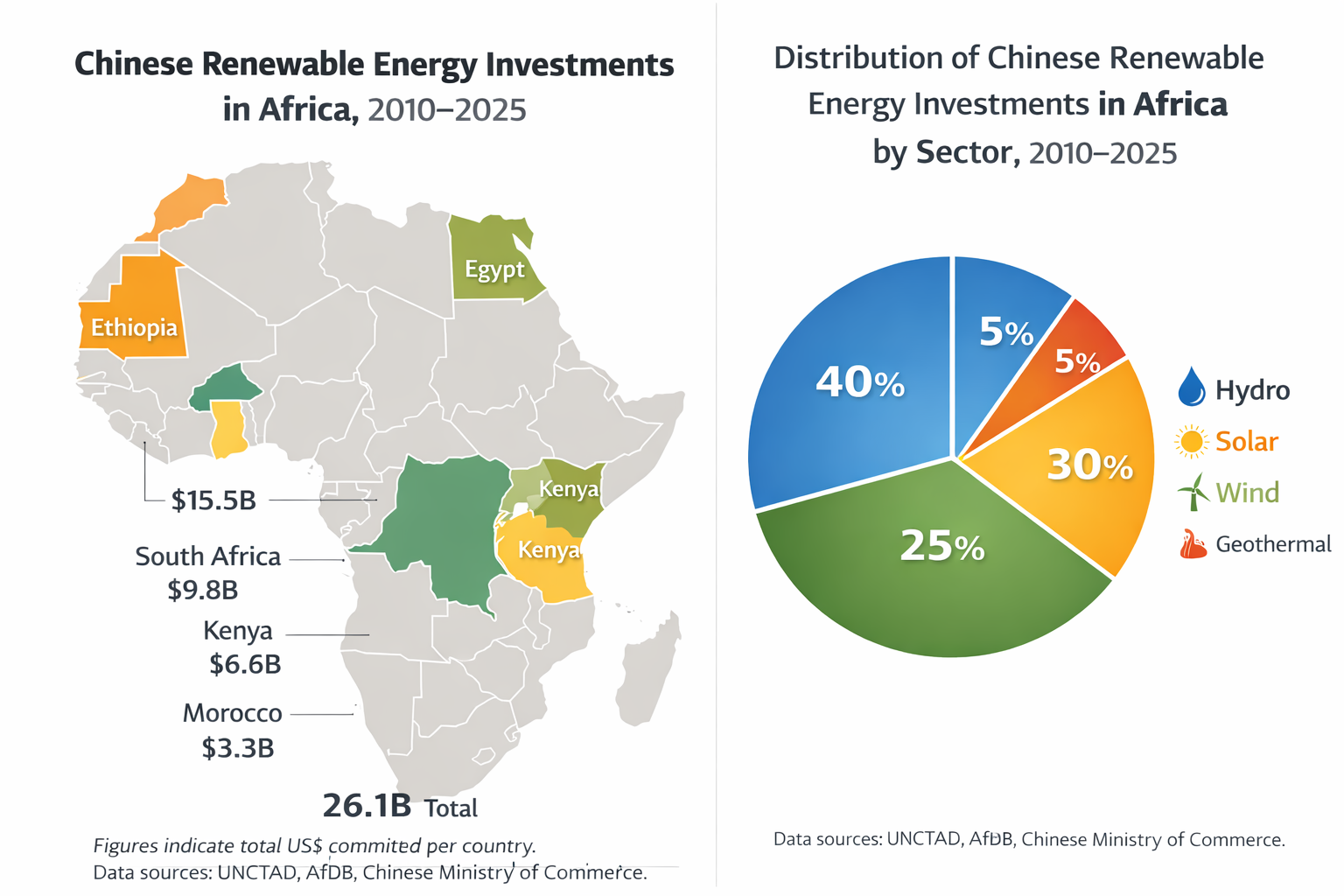

Chinese renewable energy investments in Africa, 2010–2025. Left: Total investment per country in US$ billions, highlighting Ethiopia, South Africa, and Kenya as top recipients. Right: Sectoral allocation showing hydropower, solar, wind, and geothermal shares. Data sources: UNCTAD, African Development Bank, China Development Bank

Costs, Capacity, and Real Projects: Africa’s Renewable Build‑Out

To assess China’s role in Africa’s green transition, it’s essential to examine actual projects, their costs, capacities, partners, and timelines, not just trends.

Kenya - Garissa Solar Power Plant (2018–2019)

One of the most cited examples of China’s renewable involvement is the Garissa Solar Power Plant in Kenya. Built by China Jiangxi International and financed with a US$135.7 million loan from the Export‑Import Bank of China, the 54.6 MW facility was connected to the national grid in late 2018 and commissioned in 2019. It now contributes around 2 % of Kenya’s national energy mix, powers roughly 70,000 homes, and reduces an estimated 43,000 tones of CO₂ emissions annually.

The cost per installed megawatt for this project (approximately US$2.5 million per MW) reflects both the high upfront capital expense of solar deployment in Africa and the concessional financing model that Chinese policy banks tend to use. Beyond the plant itself, the project has enabled Kenya to diversify its energy portfolio and reduce reliance on expensive fossil fuels.

Ethiopia- Adama Wind Farm (2012–2015)

In Ethiopia, Chinese financing has supported wind power expansion through the Adama Wind Farm, which consists of two phases funded largely by China Exim Bank. Valued at around US$460 million, the project delivers 204 MW of capacity: Adama I at 51 MW (commissioned 2012) and Adama II at 153 MW (commissioned 2015).

This investment contributed significantly to diversifying Ethiopia’s energy mix, which historically relied heavily on hydropower. As of recent national data, renewable sources including wind and hydropower comprise close to 90 % of Ethiopia’s installed capacity, a remarkable transformation over a decade of investment.

South Africa - Wind and Solar Supply Chains (2017–2024)

South Africa’s renewable expansion illustrates a different pattern: here, Chinese firms have focused on equipment supply and joint ventures, rather than unilateral project financing. Chinese manufacturers such as Trina Solar, BYD, and JA Solar supply panels, inverters, and battery systems for utility‑scale solar farms and wind facilities. According to industry reports, Chinese companies were involved in 11 out of 13 renewables projects completed between 2010 and 2024.

One notable example is the De Aar Wind Farm (244.5 MW), commissioned in 2017 under a joint venture involving Longyuan Power (China), reflecting how Chinese technology plays a critical role even when multilateral and local financing leads investment.

Botswana - Jwaneng Solar Power Station (2025)

In southern Africa, the Jwaneng Solar Power Station in Botswana is an example of emerging Chinese‑backed investment in solar. Construction beginning in 2024, the 100 MW project is projected to cost about US$78.3 million, financed and operated through a consortium including Chinese partners and local utilities.

Broader Financial Patterns and Export Dynamics

China’s influence in African renewable energy goes beyond individual project financing. Trade and manufacturing data show Chinese renewable technology has flooded African markets:

- In May 2025, African solar panel imports from China reached 1.57 GW in a single month, a record high, with at least 22 African nations doubling imports year‑on‑year, according to Chinese customs data analyzed by independent energy analysts. This import surge reflects both utility‑scale and off‑grid deployment trends.

- Between 2010 and 2024, a UK think tank estimates China’s energy sector involvement including renewables in Africa at approximately US$66 billion, of which a significant portion since 2018 supports solar and wind deployment.

Despite this, Africa still receives a disproportionately low share of global clean energy investment only about 3 % annually, far short of the US$200 billion per year estimated as necessary to meet energy access and climate goals across the continent.

Strategic and Development Implications

Affordable Power and Emissions Reductions

Chinese investment has helped lower the cost of renewable energy deployment in Africa. Projects like Garissa and Adama deliver clean power at scale, reducing dependence on expensive diesel generators and imported fossil fuels. This has direct implications for economic competitiveness and climate resilience in countries where grid reliability was once a major constraint.

Energy planners in Kenya and Ethiopia now factor renewable capacity into national energy strategies aimed at reducing costs for households and industry, stabilizing supply, and cutting carbon emissions. These shifts also align with broader African Union goals to expand renewable capacity from below 60 GW in 2022 to more than 300 GW by 2030 a transformative scale‑up for the continent.

Industrial Dependency and Local Value Chains

Despite positive growth, China’s dominance in equipment supply also exposes Africa to dependency risks. Most solar panels, turbines, and storage systems continue to be imported from China, with limited local manufacturing capacity developed in Africa itself. A record spike in imports such as the 1.57 GW of Chinese panels in May 2025 underscores both demand and dependency.

This dynamic has spurred debate among African policymakers about the balance between immediate cost‑effective deployment and long‑term local industrial development. Some governments are exploring policies to encourage local assembly or manufacturing, but progress remains uneven.

Debt and Finance Challenges

While renewable projects tend to have lower operating costs, their upfront capital requirements remain significant. Policy bank loans from China Exim Bank and the China Development Bank helped bridge financing gaps, but they also contribute to long‑term external liabilities for host countries. Balancing development finance with fiscal sustainability remains an ongoing challenge for many African states.

Conclusion: A Nuanced Legacy

China’s involvement in African renewable energy is far from a simple story of charity or extractive diplomacy turned green. It is a complex partnership shaped by political commitment (via FOCAC), industrial capacity, strategic export interests, and African demand for affordable, reliable electricity. Projects like Kenya’s Garissa Solar Plant (US$135.7 million) and Ethiopia’s Adama Wind Farm (US$460 million) are just visible markers of a much broader dynamic.

China’s renewable footprint has helped expand Africa’s clean energy capacity, reduce emissions, and lower power costs. Yet it also raises important questions about local industrialization, long‑term debt exposure, and the depth of technology transfer. As Africa pursues its ambitious clean energy goals, understanding the full cost, impact, and implications of Chinese investment will be essential for informed policy choices and equitable development outcomes.

{kind=link}